The risk of investing

Why investing is the new saving

Saving in a savings account or saving with investing – which is riskier? The answer to this question seems clear. Investing, logical, isn’t it? In reality, however, it is not so clear, but depends on the assessment period: in the short term you are safer with the savings account, but in the long term it looks different.

In this article we explain why this is the case and shed light on the role played by low interest rates and inflation. And we show you what influences the risk when investing and how you can significantly reduce the risk of investing with the right behaviour.

Saving in the savings account – money safely stored, but certainly not saved

Putting money aside is important. We learned that as children. So at home we diligently filled our savings box until it was full at some point and we went to the bank with it. While saving is still important, there is one important difference compared to the past: there is hardly any interest or even negative interest on savings accounts any more. This is also not simply a trend that will soon pass – rather, we have to expect interest rates to remain low.

The good thing about a savings account: You can be sure that your savings will still be there in a few years, so there is basically no risk. And if the bank should go bankrupt, your money is protected up to CHF 100,000 by the deposit guarantee. However, your money doesn’t just sit there in the savings account, but is used by the bank to grant loans and mortgages. Until you withdraw your money again, it is not working for you, but for the bank.

Long-term loss of value due to inflation

If you leave your savings in a savings account for a longer period of time, you will be at a significant disadvantage: due to inflation, your savings will lose more and more of their value. This means that while the money remains more or less the same amount on paper over the years (depending on the interest you receive), at the same time the prices of various goods slowly rise on average. This means that at some point you can buy less with your money than when you put it aside. Or even more in technical language: Due to inflation, the money in the savings account remains the same in nominal terms, but loses value in real terms. Storing money in a savings account for a longer period of time is therefore equivalent to a gradual but certain destruction of money.

Definition of inflation

“General and continuous rise in prices, or in other words, persistent loss in the value of money. There are numerous methods of calculating inflation. Most commonly, inflation is measured by the increase (expressed as a percentage) in the annual average of the national consumer price index (CPI).” – Federal Statistical Office

As the table below shows, inflation in Switzerland over the last five years, measured by the national consumer price index (CPI), has not been that high, and has even been negative in the meantime, which corresponds to a price reduction. In fact, however, inflation is much higher than these figures suggest. This is because they only include consumer goods, not assets such as shares and real estate (NZZ).

Average annual inflation in Switzerland

National Consumer Price Index (CPI) – Swiss Federal Statistical Office

Influence of monetary policy

Let us return to interest rates. The persistently low interest rates are the result of the expansive monetary policy of the national and central banks. They keep putting more and more money into circulation. This leads to a strong increase in share prices and also real estate prices and is the reason why inflation, as mentioned, is actually stronger than the CPI suggests.

The main beneficiaries of such a monetary policy are those who have invested their money, which is still mainly the wealthy. The less wealthy, on the other hand, usually have a large part of their savings in savings accounts, where they receive poor interest rates and automatically incur losses in the current environment. This redistribution could lead to a greater social gap (NZZ).

Investing money – fluctuations are unavoidable, but the risk can be greatly reduced in the long term.

Let’s now take a look at how safe it is if you don’t leave your money in a savings account, but invest it instead. The big difference with a savings account: The value of your money is subject to fluctuations when you invest it. In the short term, the mood on the stock market plays a role, which is strongly influenced by financial news and other reports. But also in the medium term, the markets fluctuate over larger cycles of about 3 years. This means that there are certainly times when you lose money (on paper) or are even in the red. And there is definitely the risk of a complete loss if, for example, you bet on the wrong companies that go bankrupt and your shares are then worth nothing. So investing is particularly risky if you depend on the success of individual companies or even sectors or countries. But you can easily counteract this.

Invest broadly with ETFs

Never before has it been as easy and inexpensive as it is today to be invested in almost every listed company in the world and thus own a tiny share of the entire global economy. How does this work? With ETFs (exchange-traded funds), which pool the money of many investors and invest it together.

How do ETFs work?

ETFs are based on an index, for example the Swiss Performance Index (SPI), which represents the Swiss stock market. The ETF pools the money of many investors and uses it to buy all the shares of the companies in the index. If you own an ETF share, you automatically own a small share of all these shares.

Investing with ETFs is considered a passive investment strategy. Since ETFs basically track an index 1:1, they also achieve the same return as the index. This contrasts with actively managed funds, which attempt to achieve a higher return than the benchmark index by focusing on particularly promising investments. However, active management incurs many costs. For this reason, most active funds demonstrably fail to outperform the benchmark after all costs have been deducted, especially over the long term.

With ETFs you do not speculate on the success of individual companies, but automatically invest very broadly in entire markets. Due to such a strong diversification, individual (small) companies in the ETF could even go bankrupt and you wouldn’t even really notice it.

But the value of ETFs also fluctuates. So you should always be aware that fluctuations are part of the investment process. It may well be that your investments lose value over several months or even years, or even fall sharply within a few days. Major temporary losses in value of around a quarter of your investment sum are quite possible and must be endured. Because the loss only really becomes a loss when it is realised, i.e. when you sell your investments.

How broadly diversified are you with findependent?

With a findependent investment solution you have shares in up to 11 ETFs, each of which covers an entire bond, equity or real estate market. This means that with as little as CHF 500 you can invest in more than 3,000 individual assets worldwide.

The risk also depends on you

In order to be able to hold on to your investments and not have to sell them at an unfavourable time, two points are crucial:

- Only invest as much money as you are sure you will not spend in the next 5 years or so. After all, you don’t want to have to sell your investments at a bad time because you are no longer liquid enough. Always keep a nest egg of around 3-6 months’ wages in your savings account.

- The more shares you have in your investment solution, the more their value fluctuates. The more shares, the higher the expected long-term return, but also the temporary loss in bad times. Bonds, on the other hand, provide stability. By choosing the right mix in your investment solution, you also control the risk. Choose an investment solution that you feel comfortable with. There’s no point in going for maximum returns if you can’t sleep peacefully in a crisis.

How do I find the right investment solution with findependent?

findependent offers five ready-made investment solutions, each with a different allocation between the asset classes equities, bonds and real estate. They range from ” cautious” with 40% equities to “adventurous” with 98% equities.

When you open an account, we use a questionnaire to determine which of these five findependent investment solutions is suitable for you. You can accept our proposal or choose another one.

Long-term increase in value and decrease in risk

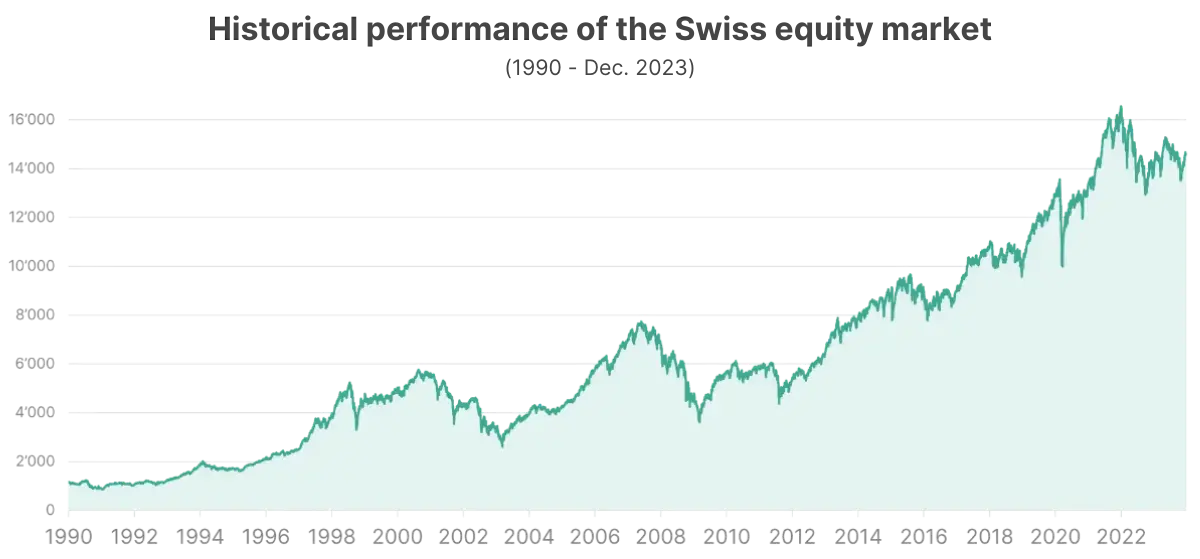

You can reduce the risk not only with a highly diversified investment solution, but also by holding your investments for a long time. If you look at how the stock markets have developed in the past, you can see a clear upward trend beyond the fluctuations. The reason for this is the general, worldwide economic growth, which leads to an increase in corporate profits and thus in the value of companies and shares. This trend leads to significant increases in value in the long term.

As an example, let’s look at the development of the Swiss stock market and see that its value has increased about fifteenfold in the last 30 years despite several phases of crisis. This shows: For investment success, it was neither necessary to predict the best stocks nor to hit the right buying and selling times. It was much more important to have a sufficiently long investment period and thus to hold the investments during all market situations.

By investing, you make more out of your savings in the long term and protect yourself against inflation. The risk of making a loss therefore decreases significantly over time, even with a broadly diversified investment solution.

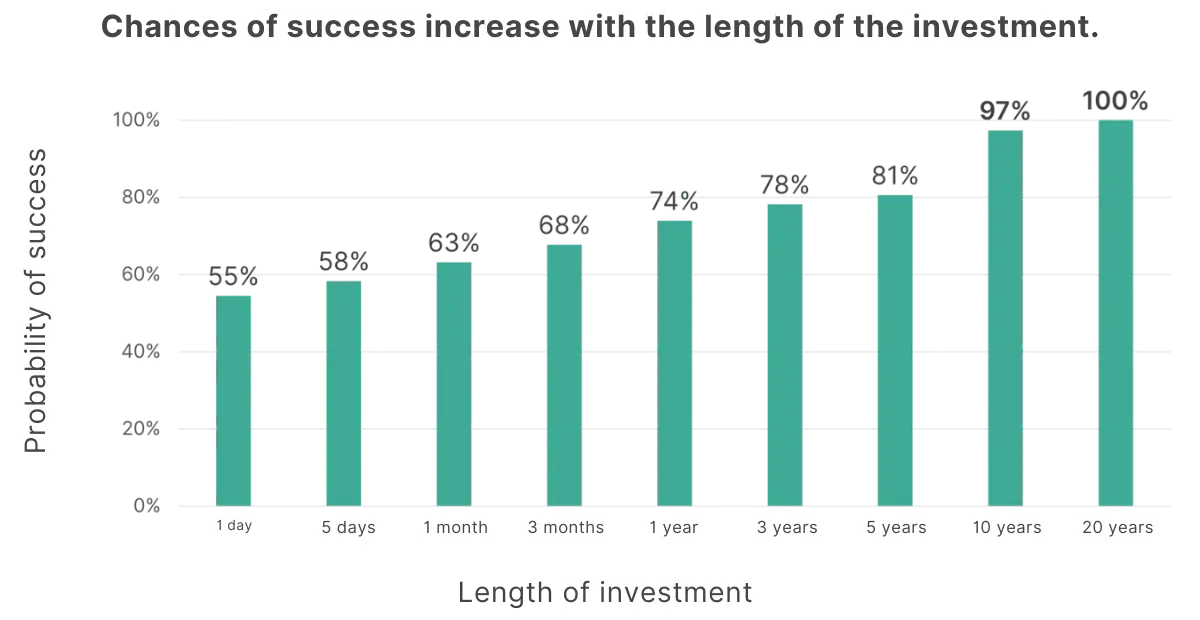

The graph below illustrates this very well. It shows the probability of success (not making a loss) if you had invested in the Swiss stock market on any given day over the last 30 years and held the investment for different investment periods.

As you can see, if you invest for just one day, the probability of winning is not much better than 50:50. You can go straight to the casino. With a longer investment period, however, this changes significantly. At around 10 years, the probability of success is already very close to 100%, and at 20 years, success is guaranteed.

Protection in the event of bankruptcy of the bank or asset manager

Last but not least, we would like to take a brief look at the risk of what would happen in the event of bankruptcy of the bank or asset manager with which you invest your money. On the one hand, as with a savings account, you have a deposit guarantee of CHF 100,000 for the liquidity portion of your investment solution. Secondly, investments are legally special assets and would not flow into a possible bankruptcy estate. In the event of bankruptcy, you could therefore still sell your investments or possibly transfer them to another deposit account.

Conclusion

In summary, investing money over a period of less than 3 years is clearly riskier than having it in a savings account. This is because the value of investments fluctuates strongly and cyclically in the short term, while the value in a savings account remains roughly constant. From an investment horizon of between 5 and 10 years, on the other hand, the risk decreases sharply with a broadly diversified investment. And while rising share prices increase the invested money and thus protect it from inflation, the purchasing power of the money in the low-interest savings account decreases.

So in the long run, investing is not really more risky than leaving money in a savings account, but it is much more rewarding. For small savers in particular, it would therefore be important to protect themselves for the future by investing. With the right investment solution, nothing stands in the way.

Note: At the moment, neither all pages nor the complete onboarding are available in English. However, we are working intensively to change this. Thank you for your understanding.

Investing money webinar

We hold regular webinars to explain the principles of investing money simply and give concrete tips for the next steps. Register here.

You might also be interested in

https://findependent.ch/wp-content/uploads/2025/02/findependent_pensionskassengeld_anlegen_vorschau_update.webp

444

668

Kay

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2025-02-04 17:34:362026-01-28 18:24:59Investing pension fund money

https://findependent.ch/wp-content/uploads/2025/02/findependent_pensionskassengeld_anlegen_vorschau_update.webp

444

668

Kay

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2025-02-04 17:34:362026-01-28 18:24:59Investing pension fund money https://findependent.ch/wp-content/uploads/2024/12/findependent_blog_vorschau_renditevergleich.webp

444

668

Kay

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2024-12-23 17:02:062025-01-22 18:16:56How to compare returns

https://findependent.ch/wp-content/uploads/2024/12/findependent_blog_vorschau_renditevergleich.webp

444

668

Kay

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2024-12-23 17:02:062025-01-22 18:16:56How to compare returns https://findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_in_krisenzeiten_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-08-07 16:51:262026-04-02 13:10:04Investing in times of crisis

https://findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_in_krisenzeiten_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-08-07 16:51:262026-04-02 13:10:04Investing in times of crisis https://findependent.ch/wp-content/uploads/2023/09/findependent_nachhaltig_anlegen_mit_findependent_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-21 18:24:562025-07-30 10:59:28Sustainable investing with findependent

https://findependent.ch/wp-content/uploads/2023/09/findependent_nachhaltig_anlegen_mit_findependent_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-21 18:24:562025-07-30 10:59:28Sustainable investing with findependent https://findependent.ch/wp-content/uploads/2023/09/findependent_lohnt_sich_ein_wechsel_der_anlageloesung_blog_banner.png

444

668

Kay

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2023-06-21 17:36:282026-01-28 17:57:17Is it worth changing investment solutions?

https://findependent.ch/wp-content/uploads/2023/09/findependent_lohnt_sich_ein_wechsel_der_anlageloesung_blog_banner.png

444

668

Kay

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2023-06-21 17:36:282026-01-28 17:57:17Is it worth changing investment solutions? https://findependent.ch/wp-content/uploads/2023/09/findependent_notgroschen_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-09 15:26:112024-12-23 13:49:30Nest egg – Looking to the future with financial security

https://findependent.ch/wp-content/uploads/2023/09/findependent_notgroschen_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-09 15:26:112024-12-23 13:49:30Nest egg – Looking to the future with financial security https://findependent.ch/wp-content/uploads/2023/09/findependent_das_kleine_1_mal_1_der_boersenpsychologie_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-03 10:04:342024-12-23 14:06:32The small 101 of stock market psychology: Why investors usually do not act rationally

https://findependent.ch/wp-content/uploads/2023/09/findependent_das_kleine_1_mal_1_der_boersenpsychologie_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-03 10:04:342024-12-23 14:06:32The small 101 of stock market psychology: Why investors usually do not act rationally https://findependent.ch/wp-content/uploads/2023/09/findependent_cleveres_einzahlungs_und_anlageverhalten_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-26 13:28:362026-01-28 18:18:24Smart deposit and investment behaviour: How best to invest your money

https://findependent.ch/wp-content/uploads/2023/09/findependent_cleveres_einzahlungs_und_anlageverhalten_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-26 13:28:362026-01-28 18:18:24Smart deposit and investment behaviour: How best to invest your money https://findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_deine_anlagen_trotz_anhaltenden_kursverlusten_nicht_verkaufen_solltest_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-21 09:12:562024-07-11 14:58:185 reasons why you should not sell your investments despite persistent price losses

https://findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_deine_anlagen_trotz_anhaltenden_kursverlusten_nicht_verkaufen_solltest_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-21 09:12:562024-07-11 14:58:185 reasons why you should not sell your investments despite persistent price losses