Pension or Capital Withdrawal

Tips and Decision-making Aids

In the context of one’s own retirement, the most important question is: pension or capital withdrawal. Receiving a consistent pension for life or opting for a one-time lump sum payout of the entire capital? We have compiled the key aspects to aid in decision-making and offer concrete tips to help you find the suitable solution for you.

At the age of 64 or 65, ordinary retirement is imminent. At this juncture, the average Swiss man and woman have accumulated tens of thousands to several hundred thousand Swiss francs in so-called retirement savings in their pension fund (second pillar). This serves to maintain an adequate standard of living even after retirement, in addition to the first pillar (AHV).

For the retirement savings accumulated during their working lives, there are typically two options. Should the accrued savings in the pension fund be paid out as a lifelong pension or as a one-time capital withdrawal? One thing is clear: there is no one-size-fits-all answer. However, there is the right answer for each individual. To make the decision a little easier for you and to better weigh the pros and cons of pension or lump sum withdrawal, here are our decision-making aids and food for thought.

Factors Influencing Decision-Making

Pension

The pension fund converts the retirement savings into a pension upon retirement. For example, if the retirement savings amount to 250,000 Swiss francs and the conversion rate is 6%, this results in an annual pension of 15,000 Swiss francs (250,000 x 6%), or monthly payments of 1,250 Swiss francs.

| Age | Invested Capital in CHF | Capital Withdrawal in CHF | Annual Asset Returns in CHF | Annual Asset Returns (after taxes) in CHF |

|---|---|---|---|---|

| 66 | 234’000 | 4’680 | 4’025 | |

| 67 | 234’000 | 4’680 | 4’025 | |

| 68 | 234’000 | 4’680 | 4’025 | |

| 69 | 234’000 | 4’680 | 4’025 | |

| 70 | 234’000 | 4’680 | 4’025 | |

| 71 | 224’000 | 10’000 | 4’480 | 3’853 |

| 72 | 214’000 | 10’000 | 4’280 | 3’681 |

| 73 | 204’000 | 10’000 | 4’080 | 3’509 |

| 74 | 194’000 | 10’000 | 3’880 | 3’337 |

| 75 | 184’000 | 10’000 | 3’680 | 3’165 |

| 76 | 174’000 | 10’000 | 3’480 | 2’993 |

| 77 | 164’000 | 10’000 | 3’280 | 2’821 |

| 78 | 154’000 | 10’000 | 3’080 | 2’649 |

| 79 | 144’000 | 10’000 | 2’880 | 2’477 |

| 80 | 134’000 | 10’000 | 2’680 | 2’305 |

| 81 | 124’000 | 10’000 | 2’480 | 2’133 |

| 82 | 114’000 | 10’000 | 2’280 | 1’961 |

| 83 | 104’000 | 10’000 | 2’080 | 1’789 |

| 84 | 94’000 | 10’000 | 1’880 | 1’617 |

| 85 | 84’000 | 10’000 | 1’445 | |

| 86 | 74’000 | 10’000 | 1’273 | |

| 87 | 64’000 | 10’000 | 1’280 | 1’101 |

| 88 | 54’000 | 10’000 | 1’080 | 929 |

| 89 | 44’000 | 10’000 | 880 | 757 |

| 90 | 34’000 | 10’000 | 680 | 585 |

| 91 | 24’000 | 10’000 | 480 | 413 |

| 92 | 14’000 | 10’000 | 280 | 241 |

| 93 | 4’000 | 10’000 | 80 | 69 |

| Total revenue: | 75’840 | 65’222 |

Aspects of Pension

- Regular Income for Life

Regardless of whether you live for another 5 years or three decades after retirement, the pension fund provides a regular pension, usually in monthly payments. - No Access to Capital

The decision for the pension is irreversible. Therefore, you cannot change your mind after a few years and opt to withdraw the remaining capital. - Protection for Survivors (Widow’s, Widower’s, and Orphan’s Pensions)

As a retiree, you remain within the pension fund, thus providing entitlement to surviving spouses for widow’s or widower’s pensions, as well as orphan’s pensions for any children. The specifics of these survivor benefits vary from pension fund to pension fund, but legally, they amount to at least 60% (for spouses) and 20% (for children) of the retirement pension. - Annual Taxation as Income

The annual pension must be fully taxed as income.

Taxation of Pension

Here, you declare the annual pension in your tax return as income from pensions. This example pertains to the tax return of the canton of Zurich.

With an annual pension income of 15,000 Swiss francs, the annual tax bill increases by around 2,200 Swiss francs. Therefore, the net pension from the pension fund amounts to 12,800 Swiss francs annually.

| State and Municipal Taxes | Federal Tax | Total Taxes | Higher Tax Burden | |

| Zurich, Kt. ZH Income 44k | 2’540.00 | 152.00 | 2’692.00 | n/a |

| Zurich, Kt. ZH Income 59k | 4’514.50 | 374.00 | 4’888.50 | +2’196.50 |

| Aarau, Kt. AG Income 44k | 2’364.50 | 152.00 | 2’516.50 | n/a |

| Aarau, Kt. AG Income 59k | 4’284.70 | 374.00 | 4’658.70 | +2’142.20 |

The details of the tax calculation are based on a base income (from AHV) of 44,000 Swiss francs, the married tax rate, and half Protestant and half Roman Catholic, without taxable assets.

The numbers vary by canton and at the municipal level, and it also depends on whether the married tax rate or the individual tax rate is applied.

Pension is generally more suitable for individuals who…

- Prefer a monthly pension

- Have a relatively low AHV pension entitlement

- Do not have additional regular income

- Have a long life expectancy

- Are married to a younger partner

- Have comparatively few savings

If ongoing expenses are already covered by the AHV pension and other regular income (such as rental income from a leased property or securities yields, etc.), there may be no need for an additional monthly pension from the pension fund. In this case, lump sum withdrawal is the better option. We have summarized the aspects related to this in the next chapter.

Capital Withdrawal

With capital withdrawal, the entire retirement savings are paid into your bank account upon retirement, and you have full control over it. Of course, this also entails a certain responsibility, as the money should be managed prudently to ensure it lasts until the end of life. Therefore, it is crucial to choose a prudent, diversified, and cost-effective investment solution.

Aspects of Capital Withdrawal

- Longevity Risk or Opportunity

Even though it may sound strange, in the case of a capital withdrawal, longevity poses more of a risk. For a centenarian, the paid-out sum must last significantly longer than for someone who passes away at the age of 75. - Investment Risk

The paid-out capital can be invested profitably. However, investing the money also entails certain fluctuations in asset value and potential risks regarding the level of annual returns. - Full Control in Case of Death

The entire remaining wealth goes to the survivors and can be freely distributed. It is also possible to consider, for example, a charitable investment or other personal matters (always in compliance with legal inheritance laws). - Financial Flexibility

The large sum allows for extraordinary activities. In addition to more consumption-oriented matters such as buying a sailboat, a vacation home, or embarking on a major trip, the (partial) repayment of the mortgage can also be considered. Repaying mortgage debts is one of the most common uses of capital withdrawals. - One-time Capital Withdrawal Tax, Annual Wealth Tax

The amount accumulated in the pension fund must be taxed as income once upon capital withdrawal. However, this is separate from other income and at a reduced rate.

Taxation of Capital Withdrawal

In the canton of Aargau, the tax is calculated at 30% of the rate, but at least at a rate of 1%. In contrast, the canton of Zurich applies a pension conversion rate to determine the tax rate. Therefore, the rates are regulated differently at the cantonal level. At the federal level, the usual rate applies, but it is only 1/5 of the ordinary tax amount.

Here, you enter the lump sum withdrawal from the pension fund in the tax return. This example pertains to the tax return of the canton of Zurich.

With a capital withdrawal of 250,000 Swiss francs, the one-time tax amounts to around 15,000 Swiss francs. This leaves approximately 234,000 Swiss francs net.

| Canton | Tax Burden in Swiss Francs | % of Capital Withdrawal |

| Zurich, Kt. ZH | 15’162.20 | 6.1% |

| Aarau, Kt. AG | 16’531.80 | 6.6% |

The numbers vary by canton and at the municipal level, and it also depends on whether the married tax rate or the individual tax rate is applied.

Important:

It should be noted that when withdrawing pension funds from the 2nd and 3rd pillars in the same tax year, the amounts are added together, resulting in a higher tax rate and thus disproportionately increasing the tax burden compared to payouts in different tax years.

Capital Withdrawal is generally more suitable for individuals…

- Wanting to have control over one’s own assets

- Receiving additional income from other sources (e.g., rental income)

- Having a short life expectancy (e.g., due to illness)

- Having personal estate planning

- Having comparatively higher savings

Pension or Capital Withdrawal – What’s worth it?

Purely Tax-based Consideration

In the post-tax analysis, according to the above explanations, the pension and capital withdrawal result in 12,800 Swiss francs of pension and 234,000 Swiss francs for lump sum withdrawal.

After roughly 18 years, the retirement savings would be depleted.

(12,800 Swiss francs x 18 years and 4 months = 234,700 Swiss francs).

However, the pension fund continues to pay the annual pension.

So, in our calculation example, opting for the pension over the lump sum withdrawal is financially advantageous if one lives past the age of 83.

Consideration with Asset Returns

Opting for lump sum withdrawal allows the received capital to be invested to generate additional returns.

Let’s assume that the 234,000 Swiss francs are invested at 2% (net after all costs) annually, with returns withdrawn each year. Additionally, from the age of 70 (after 5 years of investment), 10,000 Swiss francs are withdrawn annually from the capital (e.g., for additional medical expenses).

The asset returns of 2% amount to 4,680 Swiss francs annually, pre-tax, approximately 4,000 Swiss francs annually for the first 5 years after taxes. Subsequently, the asset return decreases by 200 Swiss francs each year due to the withdrawals of 10,000 Swiss francs p.a.

After 28 years, the capital is depleted. During this time, approximately 75,000 Swiss francs of asset returns (65,000 after taxes) could be generated.

In this example, the capital from the lump sum withdrawal would last until the age of 93.

| Age | Invested Capital in CHF | Capital Withdrawal in CHF | Annual Asset Returns in CHF | Annual Asset Returns (after taxes) in CHF |

| 66 | 234’000 | 4’680 | 4’025 | |

| 67 | 234’000 | 4’680 | 4’025 | |

| 68 | 234’000 | 4’680 | 4’025 | |

| 69 | 234’000 | 4’680 | ||

| 70 | 234’000 | 4’680 | 4’025 | |

| 71 | 224’000 | 10’000 | 4’480 | 3’853 |

| 72 | 214’000 | 10’000 | 4’280 | 3’681 |

| 73 | 204’000 | 10’000 | 4’080 | 3’509 |

| 74 | 194’000 | 10’000 | 3’880 | 3’337 |

| 75 | 184’000 | 10’000 | 3’680 | 3’165 |

| 76 | 174’000 | 10’000 | 3’480 | 2’993 |

| 77 | 164’000 | 10’000 | 3’280 | 2’821 |

| 78 | 154’000 | 10’000 | 3’080 | 2’649 |

| 79 | 144’000 | 10’000 | 2’880 | 2’477 |

| 80 | 134’000 | 10’000 | 2’680 | 2’305 |

| 81 | 124’000 | 10’000 | 2’480 | 2’133 |

| 82 | 114’000 | 10’000 | 2’280 | 1’961 |

| 83 | 104’000 | 10’000 | 2’080 | 1’789 |

| 84 | 94’000 | 10’000 | 1’880 | 1’617 |

| 85 | 84’000 | 10’000 | 1’445 | |

| 86 | 74’000 | 10’000 | 1’273 | |

| 87 | 64’000 | 10’000 | 1’280 | 1’101 |

| 88 | 54’000 | 10’000 | 1’080 | 929 |

| 89 | 44’000 | 10’000 | 880 | 757 |

| 90 | 34’000 | 10’000 | 680 | 585 |

| 91 | 24’000 | 10’000 | 480 | 413 |

| 92 | 14’000 | 10’000 | 280 | 241 |

| 93 | 4’000 | 10’000 | 80 | 69 |

| Total revenue: | 75’840 | 65’222 |

If the annual asset depletion of 10,000 Swiss francs begins immediately at the start of retirement, the capital is depleted by the age of 89, and the total asset returns amount to 57,000 Swiss francs (or 49,000 after taxes).

A 2% asset return is certainly conservatively estimated. In this calculation example, our aim is to roughly equate the two options of pension or capital withdrawal in terms of risk.

Additionally, there is the risk of sequence of returns in investments. It is possible that immediately after the investment, financial markets may correct, causing the value to decrease by 20, 30, or more percent. This can have a significant impact on the development of assets with ongoing capital withdrawals. Therefore, if capital withdrawals are planned from the beginning, it is advisable not to invest the entire amount. The capital needed for the initial years should be left in the account.

Pension or Capital Withdrawal – What’s more common?

According to the Pension Fund Statistics 2022, capital withdrawals at retirement continue to be a growing trend. Once again, lump sum withdrawals increased significantly. In 2022, a total of 54,273 retirees opted for capital withdrawals, receiving a total of 13 billion Swiss francs (+15.4% compared to the previous year). The average capital withdrawal amount was 240,291 Swiss francs (+8.9%).

Source: FSO

Pension or Capital Withdrawal – How do I make the decision?

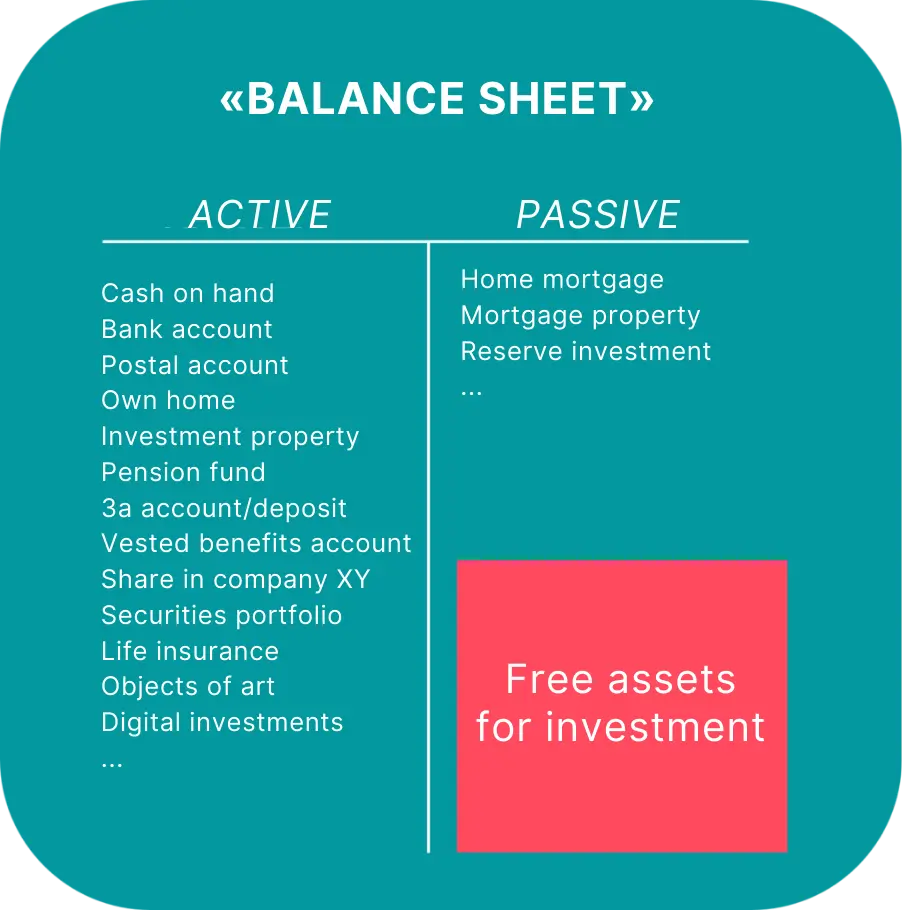

Every starting point is different and must therefore be individually assessed. As an initial aid, a budget that compares all expenses and income, as well as a balance sheet, can be beneficial.

Tips for creating the balance sheet:

- Start simply with cash and various accounts.

- For many Swiss people, their own home (always subtract the mortgage on the right) and the pension fund are the largest assets.

- It’s also important to set aside reserves for investments and major expenses.

Tips for the question of pension or capital withdrawal

- Start the evaluation process early.

- Obtain at least two different opinions from independent sources.

- Create a comprehensive and forward-looking budget to compare income and expenses.

- Take the opportunity to lay out all financial aspects.

- Be honest with yourself regarding health and life expectancy issues.

- Have experts calculate different options for you.

- If you have a substantial pension fund, consider the possibility of a partial capital withdrawal.

What to do with the capital from the Pension Fund

If you decide on a capital withdrawal, it is important to find the right investment strategy. This depends, among other factors, on the aforementioned balance sheet, budget, and your previous experiences with investments as well as your tolerance for wealth fluctuations.

Investment strategies vary in terms of investment duration, value fluctuations, and expected as well as historical returns. For findependent investment solutions, this looks as follows:

We are happy to assist you with further questions. You can contact us via chat, phone, or email, or book a non-binding personal online consultation.

This is findependent

findependent is a FINMA-licensed asset manager. We take care of the financial markets for you and independently select the right investments for you.

We avoid expensive branches to keep fees low, ensuring that the returns on your investment solution remain primarily in your pocket. And thanks to our partner bank, you don’t have to compromise on security.

Here you can learn more about us as a team.

FAQs

What is a conversion rate? A percentage used to calculate a lifelong, annually recurring pension from the retirement savings. The “mandatory” part of your BVG balance is calculated using the current minimum conversion rate of 6.8%. This rate is set by law. Many employees also have an “extra-mandatory” portion, which earns interest differently in each pension fund. Your pension statement provides information on this.

Is the pension fund pension adjusted for inflation? No, there is no legal obligation to adjust the pension for inflation. This is in contrast to the 1st pillar AHV, where the Federal Council orders an adjustment every 2 to 3 years. However, some pension funds may adjust pensions for inflation, although this is the exception rather than the rule.

Can I withdraw part as capital and part as a pension? Depending on the pension fund, this may be possible. However, there is no legal requirement for the pension fund to allow this. It’s best to inquire with the pension fund contacts for specifics.

When do I need to decide? The deadline for applying for a capital withdrawal varies from pension fund to pension fund. Retrospective applications are usually not possible, so it’s advisable to take care of this early on.

What taxes do I have to pay on a pension or capital withdrawal? You must pay income tax on the pension every year. A one-time capital withdrawal tax is levied on the capital withdrawal. Additionally, the capital must be declared as an asset every year, and any income (dividends, coupon payments, etc.) if invested, must be taxed as income.

How is the capital withdrawal tax calculated? Taxation is separate from ordinary income and at a reduced rate. The amount depends on the canton or municipality of residence.

You might also be interested in

https://findependent.ch/wp-content/uploads/2023/09/findependent_etf_sparplan_schweiz_blog_banner.png

444

668

Kay

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2025-07-24 16:34:072026-01-28 17:52:17ETF (Exchange Traded Fund) simply explained

https://findependent.ch/wp-content/uploads/2023/09/findependent_etf_sparplan_schweiz_blog_banner.png

444

668

Kay

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2025-07-24 16:34:072026-01-28 17:52:17ETF (Exchange Traded Fund) simply explained https://findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_in_krisenzeiten_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-08-07 16:51:262026-04-02 13:10:04Investing in times of crisis

https://findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_in_krisenzeiten_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-08-07 16:51:262026-04-02 13:10:04Investing in times of crisis https://findependent.ch/wp-content/uploads/2024/06/Blogposts_Vorschau_Steuern_saeule_3b.webp

444

668

Shari Kalmar

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-08-05 10:38:042025-01-23 11:44:46How are my investments with findependent taxed?

https://findependent.ch/wp-content/uploads/2024/06/Blogposts_Vorschau_Steuern_saeule_3b.webp

444

668

Shari Kalmar

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-08-05 10:38:042025-01-23 11:44:46How are my investments with findependent taxed? https://findependent.ch/wp-content/uploads/2024/01/findependent_blogartikel_rente_oder_kapital_vorschau.webp

461

460

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-07-17 10:47:312025-12-01 15:35:28Pension or capital withdrawal

https://findependent.ch/wp-content/uploads/2024/01/findependent_blogartikel_rente_oder_kapital_vorschau.webp

461

460

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-07-17 10:47:312025-12-01 15:35:28Pension or capital withdrawal https://findependent.ch/wp-content/uploads/2022/03/findependent_fondssparplan_vorschau.webp

414

622

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-04-18 12:39:142025-01-27 11:48:45Fund Savings Plan Switzerland – How It Works

https://findependent.ch/wp-content/uploads/2022/03/findependent_fondssparplan_vorschau.webp

414

622

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-04-18 12:39:142025-01-27 11:48:45Fund Savings Plan Switzerland – How It Works https://findependent.ch/wp-content/uploads/2023/05/findependent_budget_erstellen_vorschau.webp

414

622

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-14 18:13:282026-01-28 18:07:44Creating a Budget – It’s as Easy as This

https://findependent.ch/wp-content/uploads/2023/05/findependent_budget_erstellen_vorschau.webp

414

622

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-14 18:13:282026-01-28 18:07:44Creating a Budget – It’s as Easy as This https://findependent.ch/wp-content/uploads/2023/10/findependent_blog_esg_vorschau.webp

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-14 18:12:062024-12-30 08:33:21ESG Rating: What it means for companies and investors

https://findependent.ch/wp-content/uploads/2023/10/findependent_blog_esg_vorschau.webp

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-14 18:12:062024-12-30 08:33:21ESG Rating: What it means for companies and investors https://findependent.ch/wp-content/uploads/2022/03/findependent_negativzinsen_vorschau.webp

1024

1024

Tobias Katzfuss

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Tobias Katzfuss2023-03-05 20:10:052026-02-12 11:37:33Avoiding negative interest rates in Switzerland

https://findependent.ch/wp-content/uploads/2022/03/findependent_negativzinsen_vorschau.webp

1024

1024

Tobias Katzfuss

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Tobias Katzfuss2023-03-05 20:10:052026-02-12 11:37:33Avoiding negative interest rates in Switzerland https://findependent.ch/wp-content/uploads/2023/09/findependent_anlagefonds_und_strategiefonds_was_ist_das_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 01:32:042024-12-30 08:33:21Investment fund and strategy fund – what are they?

https://findependent.ch/wp-content/uploads/2023/09/findependent_anlagefonds_und_strategiefonds_was_ist_das_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 01:32:042024-12-30 08:33:21Investment fund and strategy fund – what are they? https://findependent.ch/wp-content/uploads/2023/09/findependent_digitale_vermoegensverwaltung_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 01:07:482024-12-30 08:33:21Digital asset management – what’s behind the trend?

https://findependent.ch/wp-content/uploads/2023/09/findependent_digitale_vermoegensverwaltung_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 01:07:482024-12-30 08:33:21Digital asset management – what’s behind the trend? https://findependent.ch/wp-content/uploads/2023/09/findependent_5_tipps_fuer_die_geldanlage_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:40:352026-02-04 11:08:375 tips for investing money

https://findependent.ch/wp-content/uploads/2023/09/findependent_5_tipps_fuer_die_geldanlage_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:40:352026-02-04 11:08:375 tips for investing money https://findependent.ch/wp-content/uploads/2023/09/findependent_alles_auf_einmal_investieren_oder_schrittweise_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:23:032026-01-28 17:59:24Invest everything at once or gradually – which one is better?

https://findependent.ch/wp-content/uploads/2023/09/findependent_alles_auf_einmal_investieren_oder_schrittweise_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:23:032026-01-28 17:59:24Invest everything at once or gradually – which one is better? https://findependent.ch/wp-content/uploads/2023/09/findependent_investment_apps_in_der_schweiz_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 14:31:092025-03-03 17:39:28Investment Apps in Switzerland – a comparison

https://findependent.ch/wp-content/uploads/2023/09/findependent_investment_apps_in_der_schweiz_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 14:31:092025-03-03 17:39:28Investment Apps in Switzerland – a comparison https://findependent.ch/wp-content/uploads/2023/09/findependent_robo_advisor_schweiz_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:45:582024-12-30 08:33:21Robo advisors Switzerland: It’s that simple!

https://findependent.ch/wp-content/uploads/2023/09/findependent_robo_advisor_schweiz_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:45:582024-12-30 08:33:21Robo advisors Switzerland: It’s that simple! https://findependent.ch/wp-content/uploads/2023/09/findependent_geld_sparen_in_der_schweiz_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:44:312024-12-30 08:33:21Saving money in Switzerland – how and where?

https://findependent.ch/wp-content/uploads/2023/09/findependent_etf_sparplan_schweiz_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:41:052026-01-28 17:51:39ETF savings plan Switzerland – the easy way to build wealth

https://findependent.ch/wp-content/uploads/2023/09/findependent_geld_sparen_in_der_schweiz_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:44:312024-12-30 08:33:21Saving money in Switzerland – how and where?

https://findependent.ch/wp-content/uploads/2023/09/findependent_etf_sparplan_schweiz_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:41:052026-01-28 17:51:39ETF savings plan Switzerland – the easy way to build wealth https://findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_kurz_und_einfach_erklaert_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:59:552024-07-11 15:09:46Investing explained briefly and clearly

https://findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_kurz_und_einfach_erklaert_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:59:552024-07-11 15:09:46Investing explained briefly and clearly https://findependent.ch/wp-content/uploads/2023/09/findependent_so_vermeidest_du_die_vier_anlagefehler_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:55:262023-10-12 10:54:35How to avoid the four most common investment mistakes

https://findependent.ch/wp-content/uploads/2023/09/findependent_so_vermeidest_du_die_vier_anlagefehler_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:55:262023-10-12 10:54:35How to avoid the four most common investment mistakes https://findependent.ch/wp-content/uploads/2023/09/findependent_frueh_anlegen_lohnt_sich_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:50:472024-07-11 15:15:12Investing early pays off

https://findependent.ch/wp-content/uploads/2023/09/findependent_frueh_anlegen_lohnt_sich_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:50:472024-07-11 15:15:12Investing early pays off https://findependent.ch/wp-content/uploads/2023/09/findependent_das_risiko_von_anlegen_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:48:182024-12-23 16:19:36The risk of investing

https://findependent.ch/wp-content/uploads/2023/09/findependent_das_risiko_von_anlegen_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:48:182024-12-23 16:19:36The risk of investing https://findependent.ch/wp-content/uploads/2023/09/findependent_geld_anlegen_in_der_schweiz_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-08-17 14:54:402026-02-11 11:38:16Investing money in Switzerland

https://findependent.ch/wp-content/uploads/2023/09/findependent_geld_anlegen_in_der_schweiz_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-08-17 14:54:402026-02-11 11:38:16Investing money in Switzerland