Is it worth changing investment solutions?

You already have a strategy fund or an asset management mandate with a bank and are considering switching to a more affordable provider? We’ll show you whether it’s worth it.

A look at the custody accounts of Mr. and Mrs. Swiss shows: strategy funds and asset management mandates are frequently used instruments. So the first step has been taken, instead of letting the savings languish in the account, they have invested and continue to do so. So far, so good. However, the range of simple and, above all, most affordable investment solutions has grown noticeably in recent years. So is it worth switching to a new, innovative provider?

Since this is a comprehensive topic, we have broken the analysis into several parts.

In the first part, we discuss why expensive banking products are used so often in the first place.

The changes in recent years are the focus of the second section.

Part 3 compares the costs of traditional banking products with those of digital alternatives.

In the fourth part, we show what costs arise when switching.

Part 5 is dedicated to digital solutions and their peculiarities before we draw a brief conclusion.

The only option for a long time

Strategy funds have been popular investment products for the past 20 years. A considerable part of their popularity is based on the fact that for a long time they were almost the only way to start investing money. They were convincing due to the fact that the chosen allocation between equities and bonds could be reproduced by means of a single transaction. Strategy funds are usually available from a few thousand Swiss francs. If the fortune saved was already advanced (a few hundred thousand Swiss francs), bank client advisors usually sold an asset management mandate.

Supposedly active

The fund managers of many investment and strategy funds promise to actively manage the fortune. The weighting of the asset classes is to be adjusted to changing circumstances. On an ongoing basis and at the right time. The goal of this active investment style, in addition to justifying the additional costs, is to achieve an excess return. Outperformance is defined as income that exceeds the general average or the benchmark index. Unfortunately, this goal is rarely achieved, and we explain why in a separate blog article.

Investing money – the right decision

Leaving money in the account with little, no or even negative interest was and is not an option. Investors have therefore done everything right when they invested their savings. Two of the key success factors when investing are namely starting early and regular depositing.

Return advantage of an investment over a savings account

Parameters: Start amount 10’000 Swiss francs, monthly deposit of 300 Swiss francs for 10 years, for a total of 46’000 Swiss francs paid in.

What has changed since then?

In the second part, we look at the changed framework conditions and analyse what these changes mean for you.

Shifted customer needs

However, the customers’ demands on their bank and investment solution have changed considerably in recent years. Personal advice was recently rated as the least important in a representative and highly regarded study (rank 9 out of 9). Much more important are up-to-date, digital offers and their impeccable technical reliability. Most important of all are low fees.

Quelle: Deloitte, Swiss Affluent Clients: Building a winning proposition for a growing client segment, Juni 2023.

Changing consumer behaviour

Comparing financial solutions or their fees and costs has also become socially acceptable in recent years. What started with health insurance premiums has now reached fees for financial investments via mortgage interest rates. In addition to the actual price, availability, user-friendliness and access (in the form of the minimum investment) also play decisive roles in financial matters. Consumers can rely on the help of established comparison platforms such as Moneyland and Comparis.

Wider range of products

The financial industry has reacted to these changes and has seen the emergence of numerous new providers in recent years. They are shaking up the market with digital, user-oriented investment solutions, use low-cost instruments such as exchange-traded funds (ETFs) and are convenient to operate via smartphone.

Invest passively and cheaply with ETFs

Developments in recent years have not only brought innovative providers to light, but also new investment products such as exchange-traded index funds. (Exchange Traded Funds, ETFs).

ETFs track the return of the index, can be traded at any time (liquid) and are cheap in terms of fees. This means that more of the return remains for you. In concrete terms, this means:

- The 10 largest ETFs (passive) used in Switzerland have average total annual costs of 0.2% (TER).

- The 10 largest strategy funds (active) used in Switzerland have average total annual costs of 1.71% (TER).

What can investors learn from this? The financial information company Morningstar came to the following conclusion last spring: “…focus on fees. Compared to active funds, passive funds are…significantly cheaper, which makes them hard to beat over the long term.”

Total Expense Ratio – TER

The costs incurred for the operation and management of the ETFs (exchange-traded funds) used in the investment solution are stated as a percentage of the ETF value per year and are called total expense ratio (TER).

Passive investment with a digital provider

In order to be able to compare traditional banking products with innovative and new solutions from digital providers, the following comparisons are based on findependent investment solutions.

findependent

findependent is a fintech start-up from Aarau founded in 2019. Since the launch of the investment app in February 2021, 25’000 customers have already been acquired (as of Jan 2026).

The team consists of 10 members and is supported by a prosecution committee around Prof. Dr. Thorsten Hens from the University of Zurich and advised by an advisory board, which also includes Roland Brack (founder of brack.ch).

Cost transparency and comparison of returns

In this section we look at the costs of different investment options and also make a comparison of providers and returns.

Costs as a decisive factor

Costs are an important factor when assessing an investment solution. This is because saved fees have a direct and positive effect on the return. Even supposedly small amounts make a big difference due to the compound interest effect. The longer the investment period, the more significant the yield advantage. In the following, we divide the analysis of these return advantages into two comparisons. This is because strategy/investment funds are usually recommended by the bank advisor for assets of several tens of thousands to a few hundred thousand Swiss francs. If 100’000 Swiss francs or more are invested, an asset management mandate may also be considered.

Cost savings compared to a strategy fund

For the active management style, a strategy fund charges an annual fee of around 1.70% (1). The units of the fund are then held in a custody account, for which an additional custody fee is charged, which ranges between 0.20 and 0.50% depending on the bank. This brings the total annual costs for investors to a almost 2%.

The passive investment solution from findependent costs 0.38% annually for an investment sum of 80’000 Swiss francs and already includes the custody fees in addition to the management fees.

In addition, there are the fees of the ETFs used (TER), depending on the investment solution chosen, these add another 0.20%. The total costs are thus around 0.58% per year.

For the same gross return, the active strategy fund thus generates 1.42% less net return annually for the investor than a passive investment solution. Or to put it another way: with findependent you save 1.42% in fees every year. Assuming an investment sum of 80’000 Swiss francs, that is 1’136 Swiss francs that you can save annually.

Over 10 years, this results in a yield difference of 17’199 Swiss francs due to the compound interest effect.

| after 5 years | after 10 years | after 20 years | |

| Active strategy fund, 2% annual costs | 97’332 | 118’420 | 175’290 |

| Passive investment solution, 0.58% annual costs | 104’162 | 135’619 | 229’906 |

| Return advantage of the findependent passive investment solution | 6’830 | 17’199 | 54’616 |

Parameters: 80’000 Swiss francs invested at 6% gross return (or 4% and 5.42% net) over 5, 10 and 20 years.

1. The 10 largest investment funds have an average TER of 1.70%. In addition, issuing commissions of up to 5% could be added in individual cases.

Cost savings compared to an asset management mandate

For an active asset management mandate, an annual fee of around 1.37% (2) arises.

It is not uncommon for the bank to use (partly bank-owned) funds and structured products in addition to direct investments in equities and bonds (these would again entail significant TERs of 0.5% to 3%). For our cost comparison, however, we refrain from including these TERs, since the exact amount is not known.

The investment solution from findependent costs 0.33% annually for an investment sum of 300,000 Swiss francs and already includes the custody fees in addition to the management fee.

In addition, there are the fees of the ETFs used, depending on the investment solution chosen, these add another 0.20% (3)to the bill. However, since we also waive inclusion in the asset management mandate, we apply the same practice here.

In contrast to banks, which often also use their own expensive funds in asset management, findependent does not have its own funds or ETFs, but can independently select the best and most affordable ETFs from the leading providers. In doing so, we apply our strict selection criteria.

For the same gross return, the asset management mandate thus generates over 1% less income per year for the investor:inside than a passive investment solution. Or to put it another way: with findependent you save more than 1% in fees every year. With an investment sum of 300’000 Swiss francs, that is 3’120 Swiss francs in fee savings per year. Over 10 years, the compound interest effect results in a return difference of almost 50’000 Swiss francs.

| after 5 years | after 10 years | after 20 years | |

| Active asset management, 1.37% annual costs | 376’186 | 471’719 | 741’730 |

| Passive investment solution, 0.33% annual costs | 395’257 | 520’761 | 903’973 |

| Return advantage of findependent’s passive investment solution | 19’071 | 49’042 | 162’243 |

Parameters: 300’000 Swiss francs invested at 6% gross yield (or 4.63% and 5.67% net) over 5, 10 and 20 years.

2. According to a study by the comparison service moneyland.

3. Source: Our investment solutions in detail.

Banks now also offer passive solutions

Of course, the banks have also noticed that the expensive strategy funds and asset management mandates are no longer accepted unconditionally. They are partly reacting to the dwindling demand by launching asset management mandates with a passive character. Patrick Huber from digitalmedia.ch took a closer look at the offer of a cantonal bank.

The fact that this bank offer is also anything but cheap with a 0.9% annual fee leads him to conclude: “Projected over 5 years, the investment solution of the St. Galler Kantonalbank is 35% more expensive than findependent.” Read the whole report here.

Comparison of returns

Comparing fee levels is one relatively simple thing. To make a full and fair comparison, it is equally important to look at the actual performance of the investment strategy. After all, it is also important not to compare apples with oranges when it comes to returns. We refer once again to Patrick Huber. He took the trouble to directly compare the returns of the past years. On the one hand, there is findependent with a completely digital investment solution with ETFs and available as an app. On the other side is the St. Galler Kantonalbank with an asset management mandate that invests in passive equities and bond funds.

No compromises with digital providers

In addition to aspects such as fees and returns, the supposed lack of personal support for digital alternatives is often cited when comparing them to traditional banking products. At findependent, investors can indeed rely on personal support. Even though the basic idea of the investment app is that everyone can do everything themselves, support is available via phone, e-mail and live chat if needed. Even a visit to our offices in the old town of Aarau is possible.

| The digital alternative from findependent offers: | |

| Fees: | Clearly more affordable than classic bank products |

| Return: | Comparable to better than classic bank products |

| Personal service: | Available at any time, phone, e-mail, chat, office visit |

As mentioned, the investment app is designed for “self-service”. In concrete terms, this means that the account opening can be done completely online and independent of time and place. Conveniently from the sofa or on the road. The investment solution can also be determined (and adjusted, if necessary) directly and easily in the app, as can deposits and payouts and the investment of funds.

Savings potential through switching

Many questions have already been answered and a change seems to make sense. But what costs does such a switch entail? What is the actual savings potential and when does it start paying off for you?

What does a change cost?

A change from the previous investment to a new investment solution is usually associated with costs on both sides. On the one hand, for the reduction or liquidation of the previous one and, on the other hand, for the establishment of the new one. Of course, a change only makes sense if the costs incurred are clearly lower than the expected future savings in fees. We have put together two calculation examples for you to create transparency:

Change from strategy fund to findependent investment solution

Initial situation: You currently have 80’000 Swiss francs in a strategy fund and are considering switching to findependent.

Switching costs: The switch involves one-off costs of 440 Swiss francs. This compares with annual savings of 1,136 Swiss francs.

Switching to findependent pays off in less than 5 months.

Here are the details of the calculation:

Costs for the dissolution of the Strategy Fund

The strategy fund is returned to the bank, no stock exchange trading takes place. Therefore, no stamp duties are incurred. Individual funds charge a redemption commission.

When transferring money, the fees for payment transactions add a few Swiss francs to the bill. However, you can also avoid these fees by making a transfer yourself via online banking.

Costs for the set-up of findependent investment solution

When the investments are made, the stamp duties and the costs from the trading spreads are incurred on the one hand. In addition, there are the exchange rate fees for the portion invested in ETFs in foreign currencies (outside the Swiss franc).

| findependent Anlagelösung | |

| Stamp duties | 80’000 x 0.10% = 80 Swiss francs |

| Currency conversion fees | 80’000 x 0.20% = 160 Swiss francs |

| Trading spreads | 80’000 x 0.25% = 200 Swiss francs |

| Costs for the set-up | 440 Swiss francs |

The total cost of the switch is therefore 440 Swiss francs.

Fee savings thanks to findependent

As soon as the investment solution from findependent is set up, you benefit from the low fees. Compared to your previous solution via the bank’s strategy fund, you will achieve a saving of 1’136 Swiss francs annually (for details see here).

At a glance

Savings when switching from a strategy fund to a findependent investment solution | |

| Cost advantage in the 1st year | 696 Swiss francs |

| Cost advantage from 2nd year | 1’136 Swiss francs annually |

Change from asset management mandate to findependent investment solution

Assumption: You currently have 300’000 Swiss francs in an asset management mandate at a bank and are considering switching to findependent.

Switching costs: The switch involves one-time costs of 2’700 Swiss francs. This compares with annual savings of 3’120 Swiss francs.

Switching to findependent pays off in just over 10 months.

Here are the details of the calculation:

Costs for the termination of the asset management mandate

It is usually the case that securities from an asset management mandate cannot or can only partially be transferred to other institutions. Therefore, all securities are sold. Stamp duties of around 0.10% are incurred on the sale.

In addition, there are the costs arising from the trading spreads. These are not direct fees but return losses, but for a fair view of the total costs of a switch we do not want to neglect them and estimate the amount at 0.25%.

| Traditional banking product (Asset management mandate) | |

| Stamp duties | 300’000 x 0.10% = 300 Swiss francs |

| Trading spreads | 300’000 x 0.25% = 750 Swiss francs |

| Cost of dismantling (estimated) | 1’050 Swiss francs |

One-off costs for the set-up of the findependent investment solution

When the investments are made, the stamp duties and the costs from the trading spreads are incurred on the one hand. In addition, there are the exchange rate fees for the portion invested in ETFs in foreign currencies (outside the Swiss franc).

| findependent investment solution | |

| Stamp duties | 300’000 x 0.1% = 300 Swiss francs |

| Currency conversion fees | 300’000 x 0.2% = 600 Swiss francs |

| Trading spreads | 300’000 x 0.25% = 750 Swiss francs |

| Costs for the set-up | 1’650 Swiss francs |

The total costs for the change (dismantling and set-up) thus amount to 2’700 Swiss francs.

Fee savings thanks to findependent

As soon as the investment solution from findependent is set up, you benefit from the low fees. Compared to your previous solution via the bank’s asset management mandate, you will achieve an annual saving of 3’120 Swiss francs (for details see here).

At a glance

Savings when switching from the bank’s asset management mandate to the findependent investment solution | |

| Cost advantage in the 1st year | 420 Swiss francs |

| Cost advantage from 2nd year | 3’120 Swiss francs annually |

How do I know the cost of my current investment?

You have made an investment, but are not sure what ongoing fees are involved and whether the whole thing is a good thing? You are welcome to show us your custody account statement and we will tell you which obvious and which hidden fees are included. This will give you a good basis for deciding what is best for you and your savings in the future.

Use the possibility of a non-binding and free consultation. We look forward to meeting you.

Digital solutions

New, innovative providers and their digital solutions clearly differ from traditional banking products in certain respects. In other aspects, however, they are also very similar, for example in terms of security.

Why are digital providers more affordable than banks?

findependent is more affordable than offers from traditional banks because we do not have expensive branches and an elaborate distribution network. We pass on the costs saved in this way to our users, which leads to a higher return. The idea behind it: Customers only pay for what they actually use.

For whom are digital investment solutions suitable?

An investment app is suitable for all those who are looking for a simple, user-friendly and cost-effective solution to invest their money. And prefer to hold the reins or the app in their own hands rather than relying on a bank advisor. Thanks to passive investment strategies, this also works without any prior knowledge or financial expertise.

What about security and trust at findependent?

findependent is a young company and we are absolutely aware that trust, reliability and security are central aspects of investing money.

Security

As a FINMA-licensed investment firm, we manage your account and custody account directly at findependent. You have full control and your investment solutions are available at any time. Your investments are legally yours alone and would be protected in the event of bankruptcy of findependent.

Data protection

All data is and remains stored in Switzerland. We will never sell your data to third parties and of course we adhere to the strict Swiss data protection laws.

What our customers have to say about us

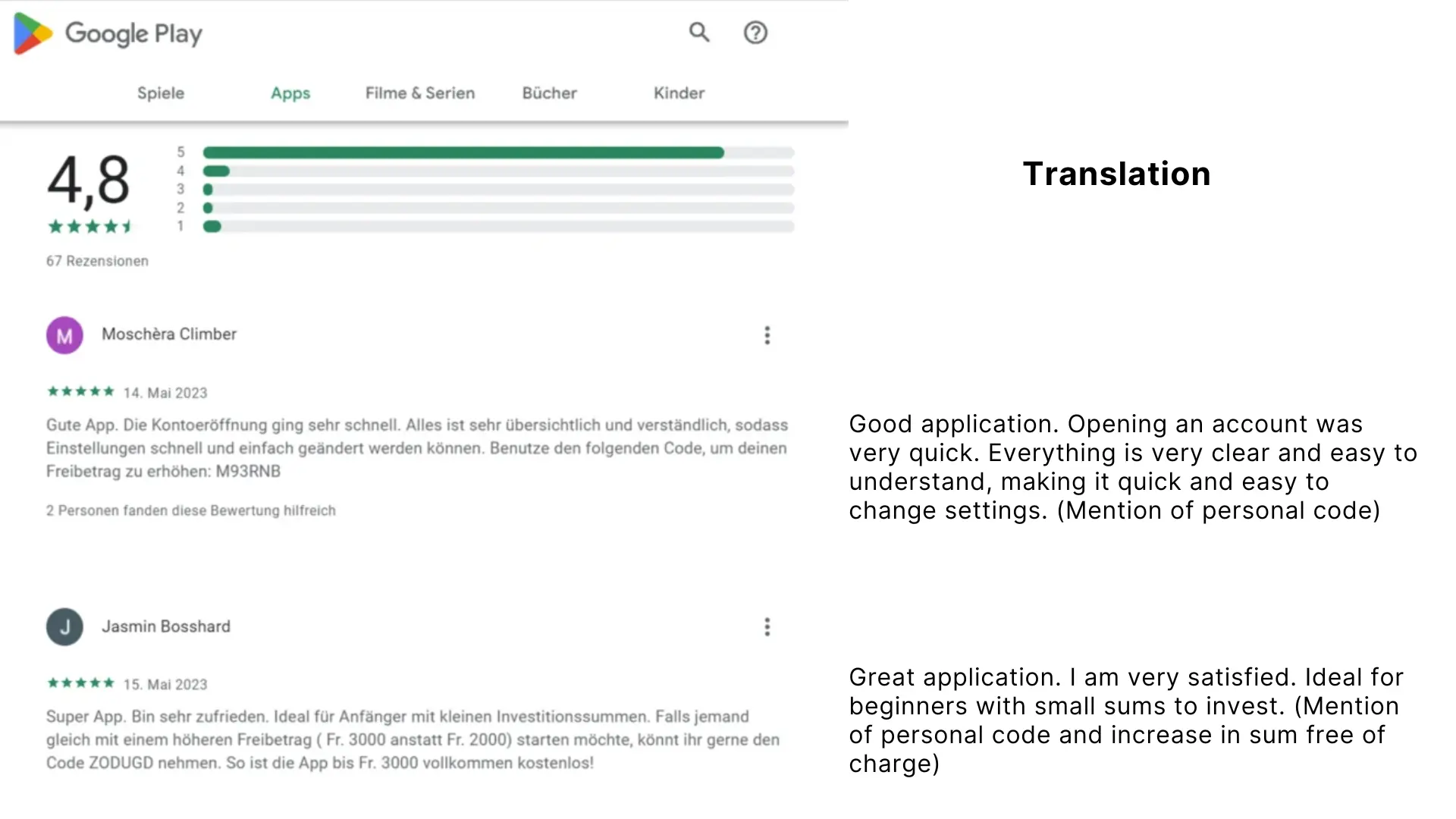

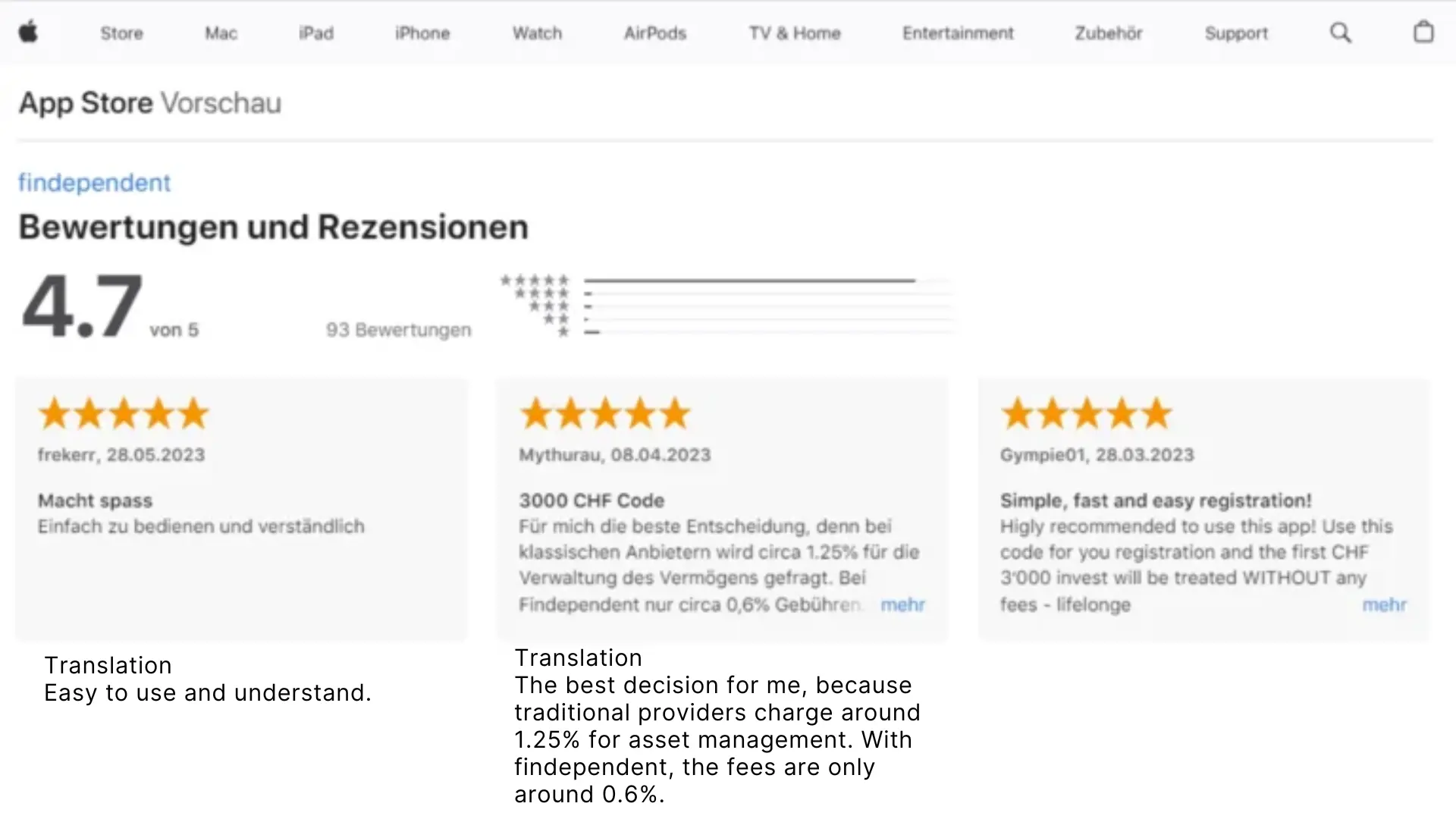

On Google, our users currently rate us with 4.9 out of 5 stars.

And the findependent investment app also does well in the App Store and the Google Play Store.

findependent advantages at a glance

Long-term success – More rewarding than bank accounts, strategy funds and asset management by a bank, because we do without expensive branches and so more remains for you.

Long-term success – More rewarding than bank accounts, strategy funds and asset management by a bank, because we do without expensive branches and so more remains for you.

Fair fees – we are completely transparent about our fees and offer one the most affordable investment app in Switzerland.

Comprehensive app – no prior knowledge is necessary and you have access at any time, regardless of location and time.

Full security – your money is in your account and custody account directly at findependent and not affected in case of bankruptcy.

Wait until you are “in the plus” again?

Is the investment you have already made currently below the cost price? Since you immediately reinvest your money using the findependent investment solution, you participate in the future price recovery. And all this at considerably more affordable fees. Every day that you pay fewer fees ultimately brings you a higher return. That’s why we recommend you don’t wait to switch.

Conclusion

Switching is associated with costs, but pays off after a couple of months.

Due to the compound interest effect, fee savings have a significant impact on the return in the long term.

You don’t have to make any compromises in terms of security, data protection and personal advice. Digital providers offer all that too.

You might also be interested in

https://findependent.ch/wp-content/uploads/2023/09/findependent_etf_sparplan_schweiz_blog_banner.png

444

668

Kay

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2025-07-24 16:34:072026-01-28 17:52:17ETF (Exchange Traded Fund) simply explained

https://findependent.ch/wp-content/uploads/2023/09/findependent_etf_sparplan_schweiz_blog_banner.png

444

668

Kay

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2025-07-24 16:34:072026-01-28 17:52:17ETF (Exchange Traded Fund) simply explained https://findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_in_krisenzeiten_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-08-07 16:51:262026-04-02 13:10:04Investing in times of crisis

https://findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_in_krisenzeiten_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-08-07 16:51:262026-04-02 13:10:04Investing in times of crisis https://findependent.ch/wp-content/uploads/2024/06/Blogposts_Vorschau_Steuern_saeule_3b.webp

444

668

Shari Kalmar

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-08-05 10:38:042025-01-23 11:44:46How are my investments with findependent taxed?

https://findependent.ch/wp-content/uploads/2024/06/Blogposts_Vorschau_Steuern_saeule_3b.webp

444

668

Shari Kalmar

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-08-05 10:38:042025-01-23 11:44:46How are my investments with findependent taxed? https://findependent.ch/wp-content/uploads/2024/01/findependent_blogartikel_rente_oder_kapital_vorschau.webp

461

460

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-07-17 10:47:312025-12-01 15:35:28Pension or capital withdrawal

https://findependent.ch/wp-content/uploads/2024/01/findependent_blogartikel_rente_oder_kapital_vorschau.webp

461

460

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-07-17 10:47:312025-12-01 15:35:28Pension or capital withdrawal https://findependent.ch/wp-content/uploads/2022/03/findependent_fondssparplan_vorschau.webp

414

622

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-04-18 12:39:142025-01-27 11:48:45Fund Savings Plan Switzerland – How It Works

https://findependent.ch/wp-content/uploads/2022/03/findependent_fondssparplan_vorschau.webp

414

622

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-04-18 12:39:142025-01-27 11:48:45Fund Savings Plan Switzerland – How It Works https://findependent.ch/wp-content/uploads/2023/05/findependent_budget_erstellen_vorschau.webp

414

622

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-14 18:13:282026-01-28 18:07:44Creating a Budget – It’s as Easy as This

https://findependent.ch/wp-content/uploads/2023/05/findependent_budget_erstellen_vorschau.webp

414

622

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-14 18:13:282026-01-28 18:07:44Creating a Budget – It’s as Easy as This https://findependent.ch/wp-content/uploads/2023/10/findependent_blog_esg_vorschau.webp

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-14 18:12:062024-12-30 08:33:21ESG Rating: What it means for companies and investors

https://findependent.ch/wp-content/uploads/2023/10/findependent_blog_esg_vorschau.webp

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-14 18:12:062024-12-30 08:33:21ESG Rating: What it means for companies and investors https://findependent.ch/wp-content/uploads/2022/03/findependent_negativzinsen_vorschau.webp

1024

1024

Tobias Katzfuss

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Tobias Katzfuss2023-03-05 20:10:052026-02-12 11:37:33Avoiding negative interest rates in Switzerland

https://findependent.ch/wp-content/uploads/2022/03/findependent_negativzinsen_vorschau.webp

1024

1024

Tobias Katzfuss

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Tobias Katzfuss2023-03-05 20:10:052026-02-12 11:37:33Avoiding negative interest rates in Switzerland https://findependent.ch/wp-content/uploads/2023/09/findependent_anlagefonds_und_strategiefonds_was_ist_das_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 01:32:042024-12-30 08:33:21Investment fund and strategy fund – what are they?

https://findependent.ch/wp-content/uploads/2023/09/findependent_anlagefonds_und_strategiefonds_was_ist_das_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 01:32:042024-12-30 08:33:21Investment fund and strategy fund – what are they? https://findependent.ch/wp-content/uploads/2023/09/findependent_digitale_vermoegensverwaltung_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 01:07:482024-12-30 08:33:21Digital asset management – what’s behind the trend?

https://findependent.ch/wp-content/uploads/2023/09/findependent_digitale_vermoegensverwaltung_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 01:07:482024-12-30 08:33:21Digital asset management – what’s behind the trend? https://findependent.ch/wp-content/uploads/2023/09/findependent_5_tipps_fuer_die_geldanlage_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:40:352026-02-04 11:08:375 tips for investing money

https://findependent.ch/wp-content/uploads/2023/09/findependent_5_tipps_fuer_die_geldanlage_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:40:352026-02-04 11:08:375 tips for investing money https://findependent.ch/wp-content/uploads/2023/09/findependent_alles_auf_einmal_investieren_oder_schrittweise_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:23:032026-01-28 17:59:24Invest everything at once or gradually – which one is better?

https://findependent.ch/wp-content/uploads/2023/09/findependent_alles_auf_einmal_investieren_oder_schrittweise_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:23:032026-01-28 17:59:24Invest everything at once or gradually – which one is better? https://findependent.ch/wp-content/uploads/2023/09/findependent_investment_apps_in_der_schweiz_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 14:31:092025-03-03 17:39:28Investment Apps in Switzerland – a comparison

https://findependent.ch/wp-content/uploads/2023/09/findependent_investment_apps_in_der_schweiz_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 14:31:092025-03-03 17:39:28Investment Apps in Switzerland – a comparison https://findependent.ch/wp-content/uploads/2023/09/findependent_robo_advisor_schweiz_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:45:582024-12-30 08:33:21Robo advisors Switzerland: It’s that simple!

https://findependent.ch/wp-content/uploads/2023/09/findependent_robo_advisor_schweiz_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:45:582024-12-30 08:33:21Robo advisors Switzerland: It’s that simple! https://findependent.ch/wp-content/uploads/2023/09/findependent_geld_sparen_in_der_schweiz_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:44:312024-12-30 08:33:21Saving money in Switzerland – how and where?

https://findependent.ch/wp-content/uploads/2023/09/findependent_etf_sparplan_schweiz_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:41:052026-01-28 17:51:39ETF savings plan Switzerland – the easy way to build wealth

https://findependent.ch/wp-content/uploads/2023/09/findependent_geld_sparen_in_der_schweiz_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:44:312024-12-30 08:33:21Saving money in Switzerland – how and where?

https://findependent.ch/wp-content/uploads/2023/09/findependent_etf_sparplan_schweiz_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:41:052026-01-28 17:51:39ETF savings plan Switzerland – the easy way to build wealth https://findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_kurz_und_einfach_erklaert_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:59:552024-07-11 15:09:46Investing explained briefly and clearly

https://findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_kurz_und_einfach_erklaert_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:59:552024-07-11 15:09:46Investing explained briefly and clearly https://findependent.ch/wp-content/uploads/2023/09/findependent_so_vermeidest_du_die_vier_anlagefehler_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:55:262023-10-12 10:54:35How to avoid the four most common investment mistakes

https://findependent.ch/wp-content/uploads/2023/09/findependent_so_vermeidest_du_die_vier_anlagefehler_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:55:262023-10-12 10:54:35How to avoid the four most common investment mistakes https://findependent.ch/wp-content/uploads/2023/09/findependent_frueh_anlegen_lohnt_sich_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:50:472024-07-11 15:15:12Investing early pays off

https://findependent.ch/wp-content/uploads/2023/09/findependent_frueh_anlegen_lohnt_sich_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:50:472024-07-11 15:15:12Investing early pays off https://findependent.ch/wp-content/uploads/2023/09/findependent_das_risiko_von_anlegen_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:48:182024-12-23 16:19:36The risk of investing

https://findependent.ch/wp-content/uploads/2023/09/findependent_das_risiko_von_anlegen_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:48:182024-12-23 16:19:36The risk of investing https://findependent.ch/wp-content/uploads/2023/09/findependent_geld_anlegen_in_der_schweiz_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-08-17 14:54:402026-02-11 11:38:16Investing money in Switzerland

https://findependent.ch/wp-content/uploads/2023/09/findependent_geld_anlegen_in_der_schweiz_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-08-17 14:54:402026-02-11 11:38:16Investing money in Switzerland