Investing is not only worthwhile for the wealthy

How to create financial freedom even with small amounts of money

«Investing is only profitable with a lot of money» is something we hear time and again. Unfortunately, many classic investment products are indeed tailored to people with a lot of assets. But for a long time now there have been offers where this is not the case. So it’s time to dispel the myth that investing is not worthwhile for small savers. Even a few hundred francs a year can make a big difference. And: With an investment solution, you don’t just make more out of your savings – you create more financial freedom and financial well-being.

Investing small amounts – an example

Of course, you shouldn’t give the shirt off your back to invest, but always leave a nest egg in your savings account. And it’s also better not to invest the money you want to spend on your next summer holiday.

But if you can save some money, it is worth investing – even small amounts! We’ll show you that right now with an example calculation.

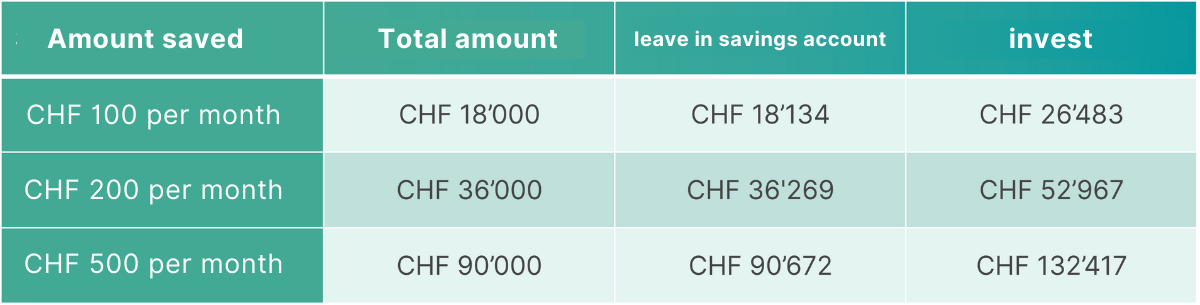

In the following table, we compare monthly investments of 100, 200 and 500 francs with savings in a savings account over an investment period of 15 years.

Comparison of investment solution vs. savings account in 15 years

Assumptions for the example: 0.1% interest on bank account, 5% return for investment solution (this corresponds approximately to the average return of the findependent investment solution “Balanced” over the last 20 years, but is no guarantee for future market developments).

You see, you get practically no interest on your savings account. And because of inflation, your money even loses value there! Basically, the main thing is not to bunker all your savings in a savings account!

This comparison also shows that it makes a real difference how much you can invest – especially over time. The question is how much you can and want to save. But it’s not just about maximising your wealth.

Calculate the yield advantage with findpendent

It’s about more than money

With an investment solution, you don’t just make more out of your savings. The cushion you save with it is much more. It means confidence that you are in a good financial position for the future. An investment solution is not only useful when you withdraw your money, but also gives you peace of mind and security today.

Investing money means that you have to do without certain things in the present, but it gives you much more freedom for your future. Whether you want to reduce your workload to have more time for family and friends, take time off to go on a world trip or buy your own house – all this can give you a good financial basis. And it also gives you the necessary security to make courageous decisions. For example, the step into self-employment is easier if you know that a smaller income will suffice in the first few years. Or if you have a good financial basis, you are more likely to quit your job and take one that pays less but is much more fulfilling.

This doesn’t mean that you should stop drinking your daily coffee or going on holiday. But you have probably found yourself spending money unnecessarily at one time or another. So spending 100 francs less per month doesn’t necessarily feel like a big sacrifice.

If you invest money regularly (and perhaps even automate it with a standing order), on the other hand, you are training yourself in a healthy habit that simply feels good.

For us, investing is also an expression of financial self-determination. You take your finances into your own hands and don’t just let your savings lie around in a savings account. There, the bank decides what your money will be used for.

What is the best way to proceed

You can invest in different ways. You can stick to a clear savings plan and pay into your investment solution every month, for example. Or you can take a more flexible approach and invest, for example, whenever you feel that enough money has accumulated in your savings account. Or you can take a closer look at your financial situation at the end of the year and then transfer money from your bank account to your investment solution.

But which of these is the smartest? Here, too, regular investment has a significant advantage. If you divide your deposits into several tranches and invest them in equal steps, you reduce the risk of having caught a bad moment in retrospect. Because it is practically impossible to recognise the “right” investment times in the present. Speculating on them is often even counterproductive – because you are always one step behind. So that you are not tempted to speculate on any point in time, you can set up a standing order.

What do I have to bear in mind for findependent?

At findependent you can start with as little as CHF 500. This amount is required at the beginning so that we can build a broad-based investment solution for you. After that, further deposits only need to amount to at least CHF 50 in order to be invested. This usually happens within 1-2 days.

In terms of costs, it makes practically no difference whether you invest often and little or rarely and more. This is because, in principle, all external costs (stamp duties, trading spreads, exchange rate surcharges for ETFs in foreign currencies) incurred when buying and selling ETFs are percentage-based. The only exception is the stock exchange levies, which amount to 0.015% but at least CHF 0.15 per ETF transaction.

Conclusion

No matter how large the amounts are, an investment pays off many times over compared to a savings account. However, an investment solution not only brings the joy of seeing your money grow in the long term, but also the certainty that you are in a good financial position. We think it’s better to forego unnecessary consumption in the present and save cleverly for the future, thus creating financial freedom for more important things in life!

If you invest your money regularly, this is smart on the one hand, because you spread your deposits over several points in time, and on the other hand, it is a good habit to be more aware of your financial future.

Note: At the moment, neither all pages nor the complete onboarding are available in English. However, we are working intensively to change this. Thank you for your understanding.

You might also be interested in

https://findependent.ch/wp-content/uploads/2025/02/findependent_pensionskassengeld_anlegen_vorschau_update.webp

444

668

Kay

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2025-02-04 17:34:362026-01-28 18:24:59Investing pension fund money

https://findependent.ch/wp-content/uploads/2025/02/findependent_pensionskassengeld_anlegen_vorschau_update.webp

444

668

Kay

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2025-02-04 17:34:362026-01-28 18:24:59Investing pension fund money https://findependent.ch/wp-content/uploads/2024/12/findependent_blog_vorschau_renditevergleich.webp

444

668

Kay

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2024-12-23 17:02:062025-01-22 18:16:56How to compare returns

https://findependent.ch/wp-content/uploads/2024/12/findependent_blog_vorschau_renditevergleich.webp

444

668

Kay

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2024-12-23 17:02:062025-01-22 18:16:56How to compare returns https://findependent.ch/wp-content/uploads/2023/09/findependent_nachhaltig_anlegen_mit_findependent_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-21 18:24:562025-07-30 10:59:28Sustainable investing with findependent

https://findependent.ch/wp-content/uploads/2023/09/findependent_nachhaltig_anlegen_mit_findependent_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-21 18:24:562025-07-30 10:59:28Sustainable investing with findependent https://findependent.ch/wp-content/uploads/2023/09/findependent_lohnt_sich_ein_wechsel_der_anlageloesung_blog_banner.png

444

668

Kay

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2023-06-21 17:36:282026-01-28 17:57:17Is it worth changing investment solutions?

https://findependent.ch/wp-content/uploads/2023/09/findependent_lohnt_sich_ein_wechsel_der_anlageloesung_blog_banner.png

444

668

Kay

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2023-06-21 17:36:282026-01-28 17:57:17Is it worth changing investment solutions? https://findependent.ch/wp-content/uploads/2023/09/findependent_notgroschen_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-09 15:26:112024-12-23 13:49:30Nest egg – Looking to the future with financial security

https://findependent.ch/wp-content/uploads/2023/09/findependent_notgroschen_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-09 15:26:112024-12-23 13:49:30Nest egg – Looking to the future with financial security https://findependent.ch/wp-content/uploads/2023/09/findependent_das_kleine_1_mal_1_der_boersenpsychologie_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-03 10:04:342024-12-23 14:06:32The small 101 of stock market psychology: Why investors usually do not act rationally

https://findependent.ch/wp-content/uploads/2023/09/findependent_das_kleine_1_mal_1_der_boersenpsychologie_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-03 10:04:342024-12-23 14:06:32The small 101 of stock market psychology: Why investors usually do not act rationally https://findependent.ch/wp-content/uploads/2023/09/findependent_cleveres_einzahlungs_und_anlageverhalten_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-26 13:28:362026-01-28 18:18:24Smart deposit and investment behaviour: How best to invest your money

https://findependent.ch/wp-content/uploads/2023/09/findependent_cleveres_einzahlungs_und_anlageverhalten_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-26 13:28:362026-01-28 18:18:24Smart deposit and investment behaviour: How best to invest your money https://findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_deine_anlagen_trotz_anhaltenden_kursverlusten_nicht_verkaufen_solltest_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-21 09:12:562024-07-11 14:58:185 reasons why you should not sell your investments despite persistent price losses

https://findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_deine_anlagen_trotz_anhaltenden_kursverlusten_nicht_verkaufen_solltest_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-21 09:12:562024-07-11 14:58:185 reasons why you should not sell your investments despite persistent price losses https://findependent.ch/wp-content/uploads/2023/09/findependent_alles_auf_einmal_investieren_oder_schrittweise_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:23:032026-01-28 17:59:24Invest everything at once or gradually – which one is better?

https://findependent.ch/wp-content/uploads/2023/09/findependent_alles_auf_einmal_investieren_oder_schrittweise_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:23:032026-01-28 17:59:24Invest everything at once or gradually – which one is better? https://findependent.ch/wp-content/uploads/2024/12/findependent_blog_passive_active_banner.webp

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 18:03:062026-01-29 15:52:00Passive or active investing – comparison and difference

https://findependent.ch/wp-content/uploads/2024/12/findependent_blog_passive_active_banner.webp

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 18:03:062026-01-29 15:52:00Passive or active investing – comparison and difference https://findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_lohnt_sich_nicht_nur_fuer_vermoegende_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:06:482024-07-11 16:38:07Investing is not only worthwhile for the wealthy

https://findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_lohnt_sich_nicht_nur_fuer_vermoegende_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:06:482024-07-11 16:38:07Investing is not only worthwhile for the wealthy https://findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_als_frau_geld_anlegen_solltest_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:03:132025-08-07 08:19:045 reasons why you should invest money as a woman

https://findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_als_frau_geld_anlegen_solltest_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:03:132025-08-07 08:19:045 reasons why you should invest money as a woman https://findependent.ch/wp-content/uploads/2023/09/findependent_wie_viel_soll_ich_anlegen_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:38:572024-07-11 17:07:21How much should I invest?

https://findependent.ch/wp-content/uploads/2023/09/findependent_wie_viel_soll_ich_anlegen_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:38:572024-07-11 17:07:21How much should I invest? https://findependent.ch/wp-content/uploads/2023/09/findependent_ist_jetzt_ein_guter_zeitpunkt_um_anzulegen_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:36:312024-07-11 15:25:48Is now a good time to invest (more)?

https://findependent.ch/wp-content/uploads/2023/09/findependent_ist_jetzt_ein_guter_zeitpunkt_um_anzulegen_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:36:312024-07-11 15:25:48Is now a good time to invest (more)? https://findependent.ch/wp-content/uploads/2023/09/findependent_groessere_betraege_anlegen_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:23:312026-02-02 22:04:22Investing larger amounts

https://findependent.ch/wp-content/uploads/2023/09/findependent_groessere_betraege_anlegen_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:23:312026-02-02 22:04:22Investing larger amounts https://findependent.ch/wp-content/uploads/2023/09/findependent_der_gender-gap_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-06-01 06:00:192025-08-07 08:23:21The Gender Investment Gap

https://findependent.ch/wp-content/uploads/2023/09/findependent_der_gender-gap_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-06-01 06:00:192025-08-07 08:23:21The Gender Investment Gap https://findependent.ch/wp-content/uploads/2023/09/findependent_inflation_laesst_ersparnisse_schmelzen_blog_banner.png

444

668

Kay

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2022-05-10 15:42:202026-02-18 16:56:21Inflation in Switzerland: How to protect your money with findependent

https://findependent.ch/wp-content/uploads/2023/09/findependent_inflation_laesst_ersparnisse_schmelzen_blog_banner.png

444

668

Kay

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2022-05-10 15:42:202026-02-18 16:56:21Inflation in Switzerland: How to protect your money with findependent