Investing money in Switzerland explained briefly and clearly – for beginners and investment professionals

Learn how and why long-term investing works

Have you ever asked yourself how the profit from investing money actually comes into being? And how does investing in Switzerland work in general? You’ll find the answers here.

How you can invest money

Investing money means using it to buy shares, bonds, real estate, gold, other commodities, cryptocurrencies, art or expensive wine. At findependent, however, we focus on investments in:

- Equities

- Bonds

- Real estate

You want to invest money in Switzerland or abroad? With findependent you do not invest directly in shares, bonds and real estate, but use exchange-traded funds, so-called ETFs. They are inexpensive and allow you to invest broadly even with little money. This makes it easier for beginners to invest money with ETFs.

How ETFs work

ETFs (“exchange traded funds”) each cover an entire market, e.g. a bond, equity or real estate market. They are therefore proven investment instruments for building up a broad-based investment solution.

ETFs are based on an index, e.g. the Swiss Performance Index (SPI), which represents the Swiss equity market. The ETF bundles the money of many investors and uses it to buy all the shares of the companies in the index. If, for example, you own a share in the “iShares SPI Core” ETF, you automatically own a small share of all the companies on the Swiss stock market.

Because you do not select individual investments but invest in an entire market, investing with ETFs is considered a passive investment strategy. Since ETFs basically track an index 1:1, they also achieve the same return as the index. This contrasts with actively managed funds, which attempt to achieve a higher return than the benchmark index by focusing on particularly promising investments. However, active management incurs many costs. For this reason, most active funds demonstrably fail to outperform the benchmark after deducting all costs, especially over the long term.

Profit from regular returns with investments

Investments in shares, bonds and real estate generate regular income, which you receive as the owner of these investments. Your invested money thus works for you. Whether you are a beginner or an expert – you don’t need to do anything else.

The three asset categories at findependent and their returns

With shares, you own shares in large companies such as Apple, Tesla or Swatch. As a result, you receive a portion of the company’s profits in the form of a dividend and benefit from the company’s long-term growth.

With bonds, you participate in large loans for governments and companies and receive regular interest payments until the entire loan is repaid at the end of the term.

With real estate, one becomes co-owner of hundreds of office and residential properties and thus earns rental income on an ongoing basis.

Income from ETFs

The ETF as the owner of the shares, bonds and real estate receives the income from these investments (dividends, interest payments, rental income). Depending on the ETF, however, this income is used differently:

- Distributing ETFs pay out the income generated, i.e. the income is effectively distributed to the ETF’s investors and transferred to their personal accounts. Findependent uses such ETFs for all Swiss investments.

- Accumulating ETFs automatically reinvest the income generated in further shares, bonds or real estate, which increases the value of the ETF. Findependent uses such ETFs for all foreign investments. Because the income does not have to be converted into Swiss francs in order to be credited to the personal account and does not have to be converted back into the foreign currency afterwards in order to be invested, one saves exchange rate costs as well as stock exchange and stamp duties.

Further explanations on the topic of distribution / accumulating ETFs can be found in this NZZ article (in German).

Investing money: What determines the price of investments

ETFs – like normal shares and bonds – can be bought and sold on the stock exchange on an ongoing basis. The price depends on supply and demand. For every buyer there is also a seller. So if more people want to buy an ETF than there are sellers on the other side, the purchase price will rise until the same number of people want to buy and sell and the market is in balance again.

But enough macro-economics 1.0, all you really need to know are the following two lines:

Number of buyers > Number of sellers ⟶ increasing prices

Number of buyers < number of sellers ⟶ decreasing prices

Investing money: Why fluctuations in value occur and are completely normal

How many people want to buy or sell depends strongly on current news and future prospects. Basically, if the forecasts are good, everyone wants to buy, if it looks bad, people are more cautious. But prices on the financial markets do not always reflect the real economic situation. A good example is the Corona crisis in 2020, in which general economic growth fell sharply worldwide, but prices recovered quickly and rose even during the crisis.

But market developments themselves also have an influence on investor behaviour: if a share rises strongly, it seems attractive and more people want to buy it. This leads to the price of the share rising further and even more people wanting to buy it. This continues until the first people start to sell the share again because they know that the price is actually much too high. The price starts to fall and now everyone wants to sell and the price falls even more.

These self-reinforcing cycles take place not only in individual stocks but also in the market as a whole and regularly lead to boom phases followed by corrections. Investment prices therefore often fluctuate in waves over several years.

Fluctuations in the value of investments are therefore part of investing. Knowing this ultimately also helps to deal well with the fluctuations in one’s own investment solution. But especially when buying investments, it is difficult not to pay too much attention to the fluctuations and not to be distracted by the current market situation. It helps to automatically make regular payments into the investment solution with a standing order instead of actively reacting to any news. If you manage to endure the fluctuations and stick to your investments in the long term, you will almost certainly profit from them.

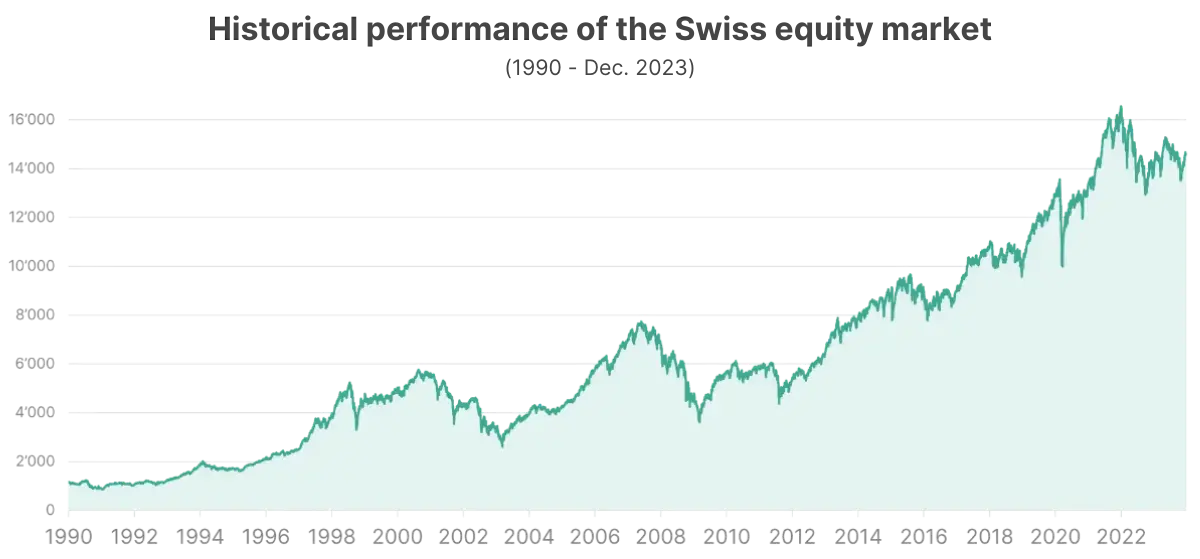

Why it pays to invest especially in the long term

Stock prices in particular rise significantly in the long term, as the chart of the Swiss stock market clearly shows.

This is because companies always pay out only part of the profit as dividends and reinvest the rest to achieve higher profits in the future. Population growth as well as technological progress mean that the global economy grows in the long term and companies thus achieve higher profits. This in turn leads to rising share prices. Real estate is also tending to become more expensive, especially in Switzerland, because land is becoming increasingly scarce.

If you hold your investments for a longer period of time, you pursue a so-called “buy and hold” investment strategy and profit from the increase in value of your investments. In contrast, daily trading is a zero-sum game with winners and losers, where you hope to hit the “right” times and quickly run the risk of speculating.

Long-term appreciation + regular returns = your profit

So if you invest your money for the long term, you benefit from long-term appreciation on the one hand and regular returns on your investments on the other. In this way, you virtually secure your fair share of global economic success. And because we at findependent are convinced that everyone should benefit from this success, we have set ourselves the goal of making investing simpler and easier to understand and thus making the associated advantages accessible to everyone.

Note: At the moment, neither all pages nor the complete onboarding are available in English. However, we are working intensively to change this. Thank you for your understanding.

You might also be interested in

https://findependent.ch/wp-content/uploads/2023/09/findependent_etf_sparplan_schweiz_blog_banner.png

444

668

Kay

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2025-07-24 16:34:072026-01-28 17:52:17ETF (Exchange Traded Fund) simply explained

https://findependent.ch/wp-content/uploads/2023/09/findependent_etf_sparplan_schweiz_blog_banner.png

444

668

Kay

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2025-07-24 16:34:072026-01-28 17:52:17ETF (Exchange Traded Fund) simply explained https://findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_in_krisenzeiten_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-08-07 16:51:262026-04-02 13:10:04Investing in times of crisis

https://findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_in_krisenzeiten_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-08-07 16:51:262026-04-02 13:10:04Investing in times of crisis https://findependent.ch/wp-content/uploads/2024/06/Blogposts_Vorschau_Steuern_saeule_3b.webp

444

668

Shari Kalmar

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-08-05 10:38:042025-01-23 11:44:46How are my investments with findependent taxed?

https://findependent.ch/wp-content/uploads/2024/06/Blogposts_Vorschau_Steuern_saeule_3b.webp

444

668

Shari Kalmar

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Shari Kalmar2024-08-05 10:38:042025-01-23 11:44:46How are my investments with findependent taxed? https://findependent.ch/wp-content/uploads/2024/01/findependent_blogartikel_rente_oder_kapital_vorschau.webp

461

460

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-07-17 10:47:312025-12-01 15:35:28Pension or capital withdrawal

https://findependent.ch/wp-content/uploads/2024/01/findependent_blogartikel_rente_oder_kapital_vorschau.webp

461

460

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-07-17 10:47:312025-12-01 15:35:28Pension or capital withdrawal https://findependent.ch/wp-content/uploads/2022/03/findependent_fondssparplan_vorschau.webp

414

622

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-04-18 12:39:142025-01-27 11:48:45Fund Savings Plan Switzerland – How It Works

https://findependent.ch/wp-content/uploads/2022/03/findependent_fondssparplan_vorschau.webp

414

622

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-04-18 12:39:142025-01-27 11:48:45Fund Savings Plan Switzerland – How It Works https://findependent.ch/wp-content/uploads/2023/05/findependent_budget_erstellen_vorschau.webp

414

622

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-14 18:13:282026-01-28 18:07:44Creating a Budget – It’s as Easy as This

https://findependent.ch/wp-content/uploads/2023/05/findependent_budget_erstellen_vorschau.webp

414

622

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-14 18:13:282026-01-28 18:07:44Creating a Budget – It’s as Easy as This https://findependent.ch/wp-content/uploads/2023/10/findependent_blog_esg_vorschau.webp

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-14 18:12:062024-12-30 08:33:21ESG Rating: What it means for companies and investors

https://findependent.ch/wp-content/uploads/2023/10/findependent_blog_esg_vorschau.webp

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-14 18:12:062024-12-30 08:33:21ESG Rating: What it means for companies and investors https://findependent.ch/wp-content/uploads/2022/03/findependent_negativzinsen_vorschau.webp

1024

1024

Tobias Katzfuss

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Tobias Katzfuss2023-03-05 20:10:052026-02-12 11:37:33Avoiding negative interest rates in Switzerland

https://findependent.ch/wp-content/uploads/2022/03/findependent_negativzinsen_vorschau.webp

1024

1024

Tobias Katzfuss

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Tobias Katzfuss2023-03-05 20:10:052026-02-12 11:37:33Avoiding negative interest rates in Switzerland https://findependent.ch/wp-content/uploads/2023/09/findependent_anlagefonds_und_strategiefonds_was_ist_das_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 01:32:042024-12-30 08:33:21Investment fund and strategy fund – what are they?

https://findependent.ch/wp-content/uploads/2023/09/findependent_anlagefonds_und_strategiefonds_was_ist_das_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 01:32:042024-12-30 08:33:21Investment fund and strategy fund – what are they? https://findependent.ch/wp-content/uploads/2023/09/findependent_digitale_vermoegensverwaltung_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 01:07:482024-12-30 08:33:21Digital asset management – what’s behind the trend?

https://findependent.ch/wp-content/uploads/2023/09/findependent_digitale_vermoegensverwaltung_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 01:07:482024-12-30 08:33:21Digital asset management – what’s behind the trend? https://findependent.ch/wp-content/uploads/2023/09/findependent_5_tipps_fuer_die_geldanlage_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:40:352026-02-04 11:08:375 tips for investing money

https://findependent.ch/wp-content/uploads/2023/09/findependent_5_tipps_fuer_die_geldanlage_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:40:352026-02-04 11:08:375 tips for investing money https://findependent.ch/wp-content/uploads/2023/09/findependent_alles_auf_einmal_investieren_oder_schrittweise_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:23:032026-01-28 17:59:24Invest everything at once or gradually – which one is better?

https://findependent.ch/wp-content/uploads/2023/09/findependent_alles_auf_einmal_investieren_oder_schrittweise_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:23:032026-01-28 17:59:24Invest everything at once or gradually – which one is better? https://findependent.ch/wp-content/uploads/2023/09/findependent_investment_apps_in_der_schweiz_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 14:31:092025-03-03 17:39:28Investment Apps in Switzerland – a comparison

https://findependent.ch/wp-content/uploads/2023/09/findependent_investment_apps_in_der_schweiz_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 14:31:092025-03-03 17:39:28Investment Apps in Switzerland – a comparison https://findependent.ch/wp-content/uploads/2023/09/findependent_robo_advisor_schweiz_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:45:582024-12-30 08:33:21Robo advisors Switzerland: It’s that simple!

https://findependent.ch/wp-content/uploads/2023/09/findependent_robo_advisor_schweiz_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:45:582024-12-30 08:33:21Robo advisors Switzerland: It’s that simple! https://findependent.ch/wp-content/uploads/2023/09/findependent_geld_sparen_in_der_schweiz_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:44:312024-12-30 08:33:21Saving money in Switzerland – how and where?

https://findependent.ch/wp-content/uploads/2023/09/findependent_etf_sparplan_schweiz_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:41:052026-01-28 17:51:39ETF savings plan Switzerland – the easy way to build wealth

https://findependent.ch/wp-content/uploads/2023/09/findependent_geld_sparen_in_der_schweiz_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:44:312024-12-30 08:33:21Saving money in Switzerland – how and where?

https://findependent.ch/wp-content/uploads/2023/09/findependent_etf_sparplan_schweiz_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 12:41:052026-01-28 17:51:39ETF savings plan Switzerland – the easy way to build wealth https://findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_kurz_und_einfach_erklaert_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:59:552024-07-11 15:09:46Investing explained briefly and clearly

https://findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_kurz_und_einfach_erklaert_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:59:552024-07-11 15:09:46Investing explained briefly and clearly https://findependent.ch/wp-content/uploads/2023/09/findependent_so_vermeidest_du_die_vier_anlagefehler_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:55:262023-10-12 10:54:35How to avoid the four most common investment mistakes

https://findependent.ch/wp-content/uploads/2023/09/findependent_so_vermeidest_du_die_vier_anlagefehler_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:55:262023-10-12 10:54:35How to avoid the four most common investment mistakes https://findependent.ch/wp-content/uploads/2023/09/findependent_frueh_anlegen_lohnt_sich_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:50:472024-07-11 15:15:12Investing early pays off

https://findependent.ch/wp-content/uploads/2023/09/findependent_frueh_anlegen_lohnt_sich_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:50:472024-07-11 15:15:12Investing early pays off https://findependent.ch/wp-content/uploads/2023/09/findependent_das_risiko_von_anlegen_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:48:182024-12-23 16:19:36The risk of investing

https://findependent.ch/wp-content/uploads/2023/09/findependent_das_risiko_von_anlegen_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:48:182024-12-23 16:19:36The risk of investing https://findependent.ch/wp-content/uploads/2023/09/findependent_geld_anlegen_in_der_schweiz_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-08-17 14:54:402026-02-11 11:38:16Investing money in Switzerland

https://findependent.ch/wp-content/uploads/2023/09/findependent_geld_anlegen_in_der_schweiz_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-08-17 14:54:402026-02-11 11:38:16Investing money in Switzerland