Invest everything at once or invest gradually?

Which one is better?

You have saved up a lot of money or received a large amount and have decided to start investing? But now you’re wondering whether you should invest all your money at once or in several steps? We will show you the advantages and disadvantages of both options. This way you can easily find the option that suits you best.

Invest all at once or invest gradually – the differences

To get an overview, here are the basic differences:

| Invest total amount at once | Invest total amount in tranches | |

| 1) | Total amount is invested over entire investment horizon | Part of the total amount is invested for less time |

| 2) | Total amount is exposed to possible price setbacks with immediate effect | Cost average effect reduces (fluctuation) risks |

| 3) | Transaction costs only arise once | Transaction fees may apply with each new investment |

| 4) | Management and custody fees apply from the start for the entire amount | Less capital causes less long management and custody fees |

| 5) | Only one money transfer necessary | Either make several payments or set up a standing order |

To better explain the individual differences, let’s take a detailed look at each one:

1) Invest once or gradually

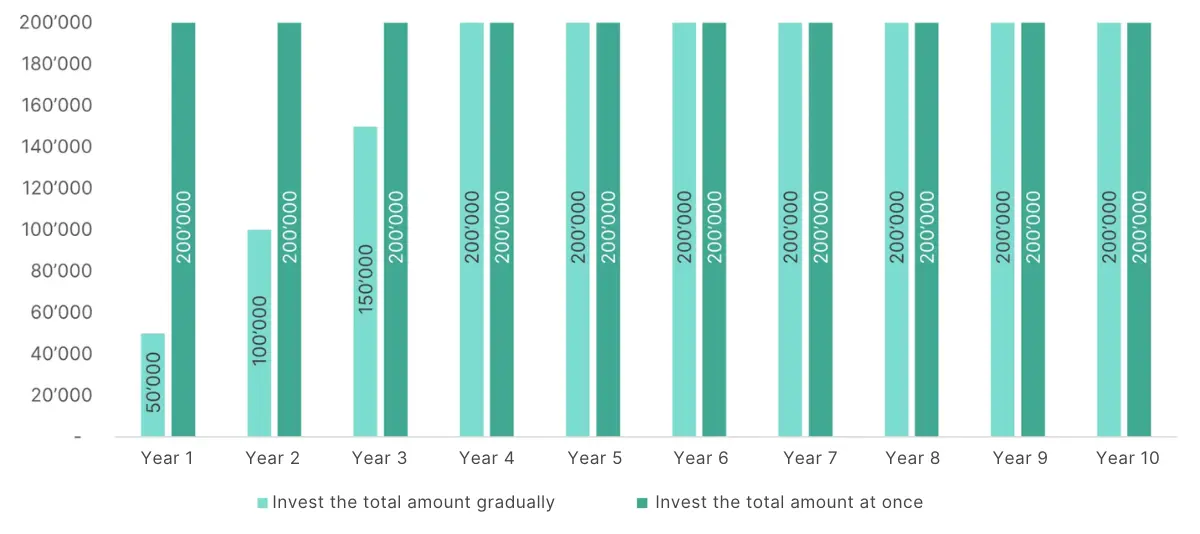

With a one-time investment, your entire capital is invested over the entire investment period. In this example, that is 200’000 francs. With a gradual investment, you invest 50’000 francs over each of the first four years.

With the one-time investment, you therefore benefit more from the compound interest effect.

The difference in return on an investment of 200’000 francs over 10 years is more than 20’000 francs, i.e. 10%.

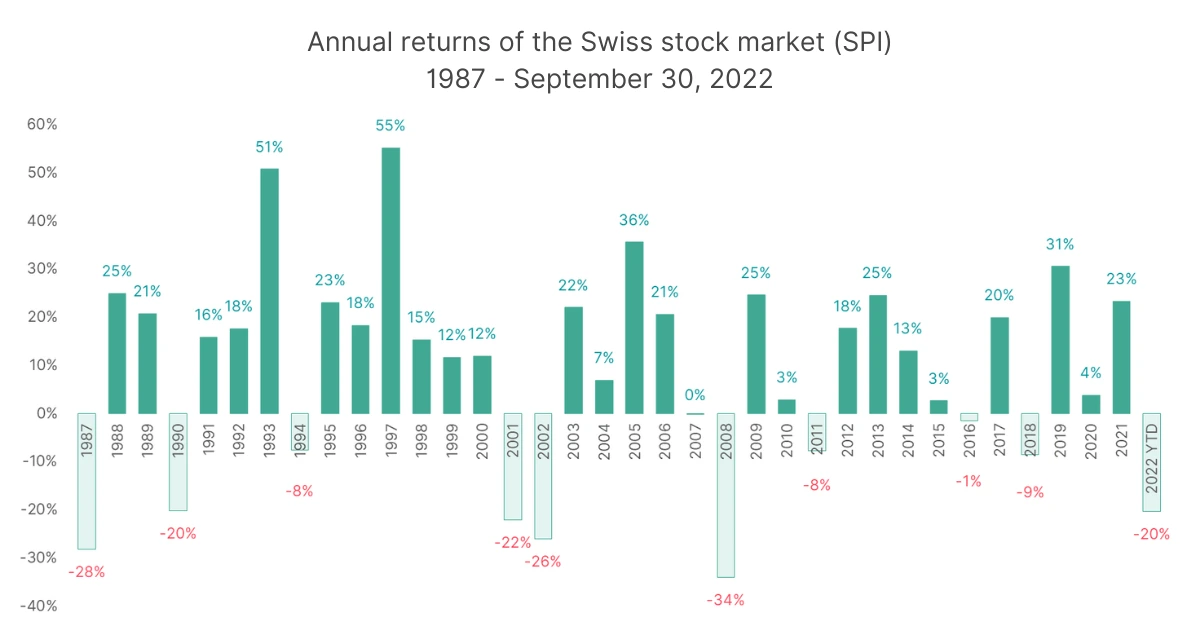

The calculations are based on the assumption that the return is 5% per year and is achieved regularly and at a constant level from the first year of investment. In reality, your investment will generate a net average annual return of around 5% over 10 years. However, there will be years with negative returns and then there will also be very good years. For example, the largest annual loss ever recorded in the Swiss stock market (Swiss Performance Index SPI) was -34% (2008), while the largest annual gain was +55% (1997).

Compound interest effect

Compound interest is interest that accrues not only on the money invested but also on the interest earned in the previous year. It helps to strengthen the performance of your investments. The longer you keep your money invested, the more the compound interest effect comes into play. Another side note: By interest we mean the return, i.e. the increase in the value of your investment.

Calculate your personal compound interest effect with our compound interest calculator.

You might also think that it’s a good time to invest money now, but that there might be an even better time in the future. However, with this approach you also accept the risk of missing out on good stock market days. This in turn has an impact on your long-term return, as the chart below shows.

However, all these calculations only work if you choose a broadly diversified and thus risk-reduced investment solution and invest for the long term (many years). If you try to do the same with a single stock, you expose yourself to the risk that exactly this stock will never fully recover from a strong price setback or that the company will even go bankrupt.

2) Possible price setbacks vs. cost average effect

Not everything always goes according to plan right from the start. Fluctuations on the financial markets can cause your investments to start correcting in the very first week and after a short time your investment solution is already in the red. Then you must not lose your head, you should keep your nerve and remain true to your long-term investment horizon.

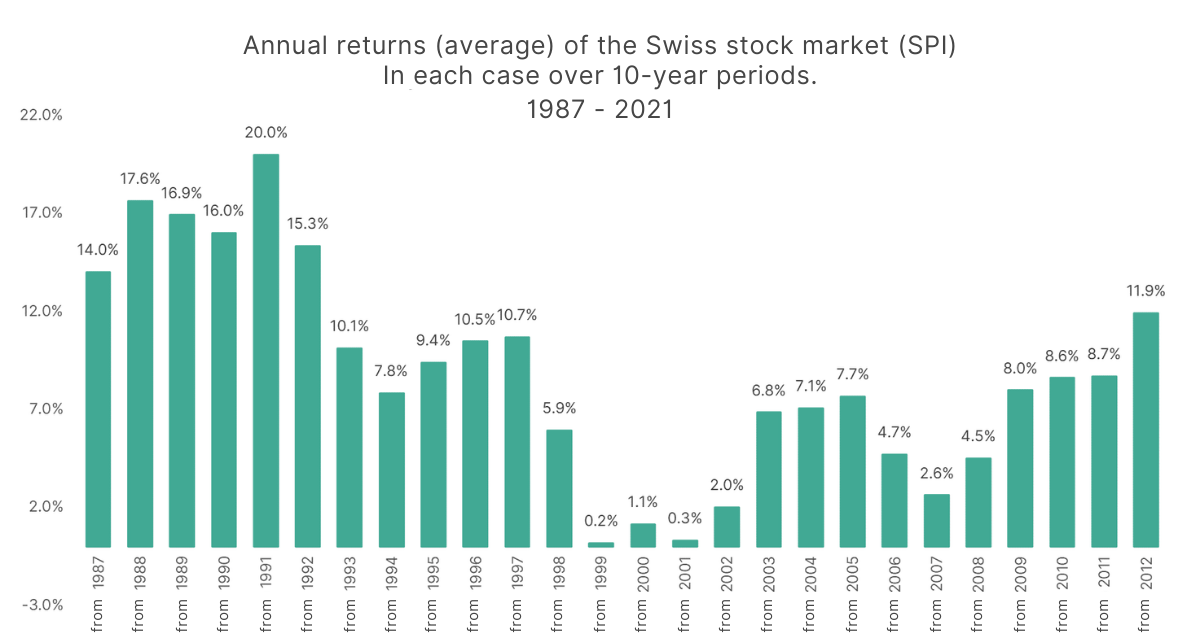

Because in every 10-year period there are time windows that deliver negative returns. The chart below shows this well.

In the long term, this will even out and you will achieve an average annual return with financial investments that is clearly higher than the interest rate on savings accounts. The price you pay for this excess return is that you accept the fluctuations in the value of your savings. The next graph illustrates well that every 10-year period, no matter when it started, has delivered a positive annual return.

However, if you decide to invest peu-à-peu, it is important that you always invest the same amount of francs (and not always buy the same number of units in a fund). With findependent, by the way, this works automatically; the total possible number of fund units is purchased with your deposit. So all you have to do is make sure you always pay in the same amount. The easiest way is by standing order.

This is particularly important in order to benefit from dollar cost averaging. It is often also called the cost average effect or smoothing effect and can be explained as follows:

For the fixed 5’000 francs you buy, for example, 50 units in the 1st quarter (100 francs per unit). Your next payment of 5’000 francs is made in the second quarter, when the units have just experienced a short-term setback of 10% (to 90 francs per unit). So for your 5’000 francs you now receive 55 units. Therefore, with regular payments, you no longer have to guess whether the financial markets are currently at a high or low. When prices are high, you automatically buy fewer shares, and when prices are low, you buy more. This smoothes out the average cost price.

We do not know with certainty what fluctuations await us. But we know with certainty that these fluctuations will occur. And we can say with a probability bordering on certainty that positive returns will be achieved in the long term. Even if it may not look that way after one, two or three years.

3) Transaction fees

Transaction fees are incurred when investing money. We are talking here about the actual transaction fees, not the annual management fees. Transaction fees are also called brokerage fees. Depending on the provider and investment solution, the amount of these fees varies significantly. Some providers reduce the amount of the transaction fee with increasing volume by means of a graduated tariff, but this graduation often only starts at several thousand or even ten thousand francs. In most cases, a minimum fee is also applied.

A numerical example: The brokerage fee at provider X for volumes up to 10’000 francs is 0.5% with a minimum fee of 40 francs. For an investment amount of 2’000 francs, not 0.5% but 40 francs are charged. In percentage terms, these 40 francs amount to a whopping 2%. So if you invest 2’000 francs 5 times in stages, you will not only incur transaction fees of 40 francs each time, but they will also be higher than for a one-off investment.

Step by step:

5 x 40 francs = 200 francs transaction fees, auf 5 x 2’000 francs investment amount this results in 2%

One-off:

10’000 francs x 0.5% = 50 francs

It would be much better to look for an investment solution that does not charge traditional transaction fees. Like the investment app from findependent.

What is incurred in any case are stamp duties and stock exchange fees, which on the one hand are relatively low at around 0.1% and on the other hand are not subject to a graduated tariff. For an investment of 2 x 10’000 francs, they are almost identical to an investment of 20’000 francs.

The findependent investment app therefore helps you to keep the fees low, even with a gradual investment. If you want to calculate exactly which fees apply for which amount, we have a calculator for you:

4) Management fees

The management fees for a professional investment are calculated on the basis of the invested assets. If you have invested 20’000 francs, for example, it is 0.4% of 20’000 = 80 francs per year (or 20 francs per quarter). If instead of investing 20’000 francs once, you invest 5’000 francs in four steps, you naturally save the management fee of 30 francs for the first three quarters.

However, you also do not participate in a possible increase in value and the compound interest effect is less effective (see point 1).

5) Administration

If you decide to make a one-off investment, the administrative effort is minimal. You give a one-time order to transfer the desired amount and when it is received in your findependent account, the investment is made in the investment solution of your choice.

If you choose to invest gradually, it is easiest to set up a standing order with your bank for the various tranches. That way you don’t have to worry about it, you certainly won’t forget to make a deposit and you won’t let your emotions get the better of you. It can happen that a temporarily bad situation on the financial markets can dissuade you from making the planned investment.

Conclusion

Now we have talked a lot about numbers, returns and yields. But when it comes to investing money, emotions also play an important role.

The question of which option is the better one is easy to answer in purely rational and mathematical terms: investing the total amount at once is usually the more successful way in the long run. But this requires strong nerves. You have to be able to cope with price setbacks, even if they occur right at the beginning.

So if you are looking for a nerve-saving variant, the step-by-step investment suits you better. Starting with smaller steps is often a recommended variant to actually become active and not to keep putting off the decision.

As long as you have not started investing, time is running against you. As soon as you are invested, time is in your favour and you benefit from the long-term positive performance.

You might also be interested in

https://findependent.ch/wp-content/uploads/2025/02/findependent_pensionskassengeld_anlegen_vorschau_update.webp

444

668

Kay

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2025-02-04 17:34:362026-01-28 18:24:59Investing pension fund money

https://findependent.ch/wp-content/uploads/2025/02/findependent_pensionskassengeld_anlegen_vorschau_update.webp

444

668

Kay

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2025-02-04 17:34:362026-01-28 18:24:59Investing pension fund money https://findependent.ch/wp-content/uploads/2024/12/findependent_blog_vorschau_renditevergleich.webp

444

668

Kay

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2024-12-23 17:02:062025-01-22 18:16:56How to compare returns

https://findependent.ch/wp-content/uploads/2024/12/findependent_blog_vorschau_renditevergleich.webp

444

668

Kay

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2024-12-23 17:02:062025-01-22 18:16:56How to compare returns https://findependent.ch/wp-content/uploads/2023/09/findependent_nachhaltig_anlegen_mit_findependent_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-21 18:24:562025-07-30 10:59:28Sustainable investing with findependent

https://findependent.ch/wp-content/uploads/2023/09/findependent_nachhaltig_anlegen_mit_findependent_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2024-03-21 18:24:562025-07-30 10:59:28Sustainable investing with findependent https://findependent.ch/wp-content/uploads/2023/09/findependent_lohnt_sich_ein_wechsel_der_anlageloesung_blog_banner.png

444

668

Kay

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2023-06-21 17:36:282026-01-28 17:57:17Is it worth changing investment solutions?

https://findependent.ch/wp-content/uploads/2023/09/findependent_lohnt_sich_ein_wechsel_der_anlageloesung_blog_banner.png

444

668

Kay

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2023-06-21 17:36:282026-01-28 17:57:17Is it worth changing investment solutions? https://findependent.ch/wp-content/uploads/2023/09/findependent_notgroschen_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-09 15:26:112024-12-23 13:49:30Nest egg – Looking to the future with financial security

https://findependent.ch/wp-content/uploads/2023/09/findependent_notgroschen_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-09 15:26:112024-12-23 13:49:30Nest egg – Looking to the future with financial security https://findependent.ch/wp-content/uploads/2023/09/findependent_das_kleine_1_mal_1_der_boersenpsychologie_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-03 10:04:342024-12-23 14:06:32The small 101 of stock market psychology: Why investors usually do not act rationally

https://findependent.ch/wp-content/uploads/2023/09/findependent_das_kleine_1_mal_1_der_boersenpsychologie_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-05-03 10:04:342024-12-23 14:06:32The small 101 of stock market psychology: Why investors usually do not act rationally https://findependent.ch/wp-content/uploads/2023/09/findependent_cleveres_einzahlungs_und_anlageverhalten_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-26 13:28:362026-01-28 18:18:24Smart deposit and investment behaviour: How best to invest your money

https://findependent.ch/wp-content/uploads/2023/09/findependent_cleveres_einzahlungs_und_anlageverhalten_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-26 13:28:362026-01-28 18:18:24Smart deposit and investment behaviour: How best to invest your money https://findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_deine_anlagen_trotz_anhaltenden_kursverlusten_nicht_verkaufen_solltest_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-21 09:12:562024-07-11 14:58:185 reasons why you should not sell your investments despite persistent price losses

https://findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_deine_anlagen_trotz_anhaltenden_kursverlusten_nicht_verkaufen_solltest_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-04-21 09:12:562024-07-11 14:58:185 reasons why you should not sell your investments despite persistent price losses https://findependent.ch/wp-content/uploads/2023/09/findependent_alles_auf_einmal_investieren_oder_schrittweise_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:23:032026-01-28 17:59:24Invest everything at once or gradually – which one is better?

https://findependent.ch/wp-content/uploads/2023/09/findependent_alles_auf_einmal_investieren_oder_schrittweise_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2023-01-09 00:23:032026-01-28 17:59:24Invest everything at once or gradually – which one is better? https://findependent.ch/wp-content/uploads/2024/12/findependent_blog_passive_active_banner.webp

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 18:03:062026-01-29 15:52:00Passive or active investing – comparison and difference

https://findependent.ch/wp-content/uploads/2024/12/findependent_blog_passive_active_banner.webp

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-12-20 18:03:062026-01-29 15:52:00Passive or active investing – comparison and difference https://findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_lohnt_sich_nicht_nur_fuer_vermoegende_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:06:482024-07-11 16:38:07Investing is not only worthwhile for the wealthy

https://findependent.ch/wp-content/uploads/2023/09/findependent_anlegen_lohnt_sich_nicht_nur_fuer_vermoegende_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:06:482024-07-11 16:38:07Investing is not only worthwhile for the wealthy https://findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_als_frau_geld_anlegen_solltest_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:03:132025-08-07 08:19:045 reasons why you should invest money as a woman

https://findependent.ch/wp-content/uploads/2023/09/findependent_5_gruende_wieso_du_als_frau_geld_anlegen_solltest_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 16:03:132025-08-07 08:19:045 reasons why you should invest money as a woman https://findependent.ch/wp-content/uploads/2023/09/findependent_wie_viel_soll_ich_anlegen_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:38:572024-07-11 17:07:21How much should I invest?

https://findependent.ch/wp-content/uploads/2023/09/findependent_wie_viel_soll_ich_anlegen_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:38:572024-07-11 17:07:21How much should I invest? https://findependent.ch/wp-content/uploads/2023/09/findependent_ist_jetzt_ein_guter_zeitpunkt_um_anzulegen_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:36:312024-07-11 15:25:48Is now a good time to invest (more)?

https://findependent.ch/wp-content/uploads/2023/09/findependent_ist_jetzt_ein_guter_zeitpunkt_um_anzulegen_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:36:312024-07-11 15:25:48Is now a good time to invest (more)? https://findependent.ch/wp-content/uploads/2023/09/findependent_groessere_betraege_anlegen_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:23:312026-02-02 22:04:22Investing larger amounts

https://findependent.ch/wp-content/uploads/2023/09/findependent_groessere_betraege_anlegen_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-09-30 15:23:312026-02-02 22:04:22Investing larger amounts https://findependent.ch/wp-content/uploads/2023/09/findependent_der_gender-gap_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-06-01 06:00:192025-08-07 08:23:21The Gender Investment Gap

https://findependent.ch/wp-content/uploads/2023/09/findependent_der_gender-gap_blog_banner.png

444

668

findependent-admin

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

findependent-admin2022-06-01 06:00:192025-08-07 08:23:21The Gender Investment Gap https://findependent.ch/wp-content/uploads/2023/09/findependent_inflation_laesst_ersparnisse_schmelzen_blog_banner.png

444

668

Kay

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2022-05-10 15:42:202026-02-18 16:56:21Inflation in Switzerland: How to protect your money with findependent

https://findependent.ch/wp-content/uploads/2023/09/findependent_inflation_laesst_ersparnisse_schmelzen_blog_banner.png

444

668

Kay

https://findependent.ch/wp-content/uploads/2024/10/test-etf-awards-5.svg

Kay2022-05-10 15:42:202026-02-18 16:56:21Inflation in Switzerland: How to protect your money with findependent